A Distressed Deal Walks Into a Bar…

Multifamily investors, operators, developers, and service providers must monitor economic indicators to make the right decisions in their real estate businesses. Want to understand if the Federal Reserve will lower interest rates? Look at U.S. Consumer Spending, U.S. Personal Consumption Index, and U.S. employment figures, to name a few. Want to learn about the long-term implications of negative interest rate policies? Look at Japan's inflation rate. Want to appreciate how the U.S. economy’s best proxy is handling inflation? Peer into the Euro-Area Inflation trends. Tracking, understanding, and analyzing all the above (and more) is laborious and time consuming; sometimes, a single good anecdote can compel decision-making in ways that data streams can't.

Below you will find a deal story that speaks to the opportunities in the market today.

10 Unit Building

Sunset Park, Brooklyn

The timeline:

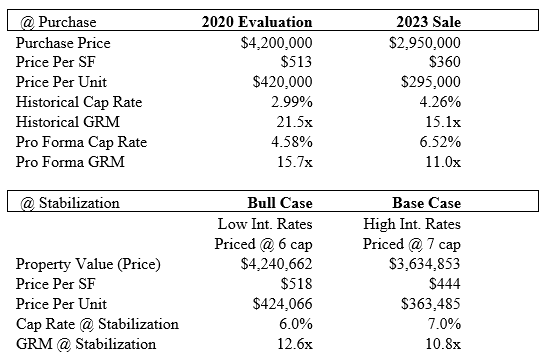

2020: I valued the property at $4,200,000

2022: I listed the property for sale at $3,900,000

2023: I sold the property for $2,950,000

This mixed-use property was in distress at the time of sale. Though it was largely free of violations, the property contained several months of property tax arrears, and some of the tenants were not paying rent. Further and notably, a few of the units in the building were vacant further reducing the gross income.

Business case: At a $2.95m price, a 31% discount to the original value in 2020, the buyer secured a basis of $295,000 per unit, with an average rent per unit of ~$1,630 per month, or ~$19,500 per year, per unit. That's a 15x GRM. With expenses per unit just under $8k, each unit makes $11,500 in net income, equal to an in-place 4.3% cap. But that's with two empty units and two non-paying tenants. On day 1, the buyer gets a 4.3% cap rate with 40% economic and real vacancy in the property. Once the purchaser leases the units and replaces the non-paying tenants – give or take a $100,000 expenditure, the building will produce close to $26,000 per unit. Expenses remain at $8k, which means the units now make about $19,000 in net income per unit. Bake in a cost of ~$100k for the clean-up of the units (renovation, removing tenants, re-leasing), and the building should yield over a 6% return at a cost basis of $3.05m.

Fast forward three years and the building could really start to thrive.

Update the residential tenant mix to obtain higher rents (from below market $1,600 to $3,000)

Retail leases come due and negotiate higher rent with existing commercial tenants (from $11,000 to $12,500)

When we consider the potential for increased revenue and the likelihood of favorable market conditions, the deal could stabilize at a yield-on-cost of close to 8%. As interest rates decrease, this could turn into a +10% cash-on-cash return. And when cap rate compression happens, the value of the building could ascend north of $4.0m.

As I have shared before:

The discounts in pricing are here.

There will be more coming, but some are here now.

They are in front of you.

I am bullish in NYC Multifamily. Call me at 212 658 1471.

Interesting piece here: https://marginalrevolution.com/marginalrevolution/2024/07/rent-control-2.html?utm_source=feedly&utm_medium=rss&utm_campaign=rent-control-2