Buying is expensive, some rents are growing, and research says building more is better

Because the cost of buying is so high, some rents continue to grow and fast.

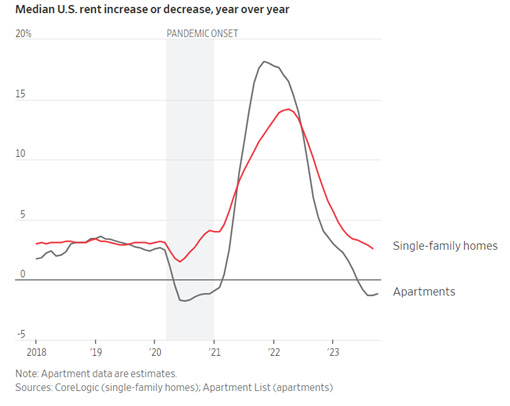

Per the chart above, single family homes continue to see rent growth, despite some headwinds in apartment rent growth. According to CoreLogic, a real estate data platform, September multifamily apartment rents declined on average by 1.3% year over year (YOY) in the U.S. Single Family Rentals (SFRs), on the other hand, saw September rents increase 2.6% YOY. Some of the large players like Invitation Homes even saw rent increases of 6% in Q3 2023, YOY. One explanation for this is that the costs of mortgages have soared to 152% of the cost of renting, according to CBRE analyses. That would entice residents to rent, but not buy. But climbing interest rates don’t explain why SFR rents are going up and multifamily rents are not.

According to analysts, tenants in single-family homes also move less often than apartment renters and may be more willing to absorb rent increases if their families feel settled in a neighborhood and school system. Further, renters of houses tend to be wealthier than apartment renters, which may further dictate that homes are chosen more carefully and for specific reasons besides price point. In other words, multifamily renters may value shop while single family renters may pay more for long term reasons like school district quality, growing communities, etc.. This might make single family renters less price elastic, and this allows investors to capitalize on rent bumps.

If rents are increasing (i.e. Invitation Homes’s portfolio), investors will enter the market to extract more (economic) rents and that means more property development. More development would satisfy the NYC government’s policy of enabling developers to provide housing and get paid for it – which is desperately needed in NYC. Still, in NYC there continue to be concerns around two major areas:

1.Do new apartments developments raise rents everywhere else (gentrification)?

A few international and local studies over the last two years suggest that building more apartments have distinctly positive effects on lowering rents for tenants long term. Here they are below, from Bloomberg’s CityLab:

In a study in Auckland, New Zealand, a 4.1% increase in housing stock led to 26% to 33% lower rents for three-bedroom units after six years.

Another study on German municipalities between 2010 and 2017 found a 1% increase in yearly new housing supply correlated with a 0.2% decrease in average rents.

One 2021 study by UC Berkeley researcher Kate Pennington studied new housing built on San Francisco lots where the prior building was destroyed by a fire. Rents in nearby buildings fell slightly compared to what they could have risen to, Pennington found, by around 1.2% to 2.3%

In New York, researcher Xiado Li’s finds that “for every 10% increase in the housing stock, rents decrease 1% and sales prices also decrease within 500 feet.”

These four independent studies highlight the positive impact that enabling new development can have on communities, from a policy perspective. On the other hand, research published by Stanford Economics Professor Rebecca Diamond highlights, albeit with some nuance, that rent controls increase rents over the longer term in communities. It’s a good idea to read the four studies that relate new development to rent declines as well as the rent control study to get a clear picture of the housing landscape.

2. Do new developments cause existing displacement?

Shiny new luxury towers emerge in neighborhoods that historically didn’t have such levels of investment tend to attract comparatively higher income, higher education people who are drawn to more amenity-having building spaces. But does that necessarily mean that lower-income folks are forced to leave in droves? That is a nuanced and difficult question to ask. There are many variables that would play a role in shaping that. Some questions that come to mind:

Are the new projects replacing occupied housing structures, or are they being built on non-residential land/properties?

Are the nearby properties subject to rent controls, effectively capping the rent increases allowed?

Are some of the units in the new project reserved for lower-income folks?

According to the UC Berkeley study performed in San Francisco, displacement risks and probabilities of receiving eviction notices within 100 feet from the new development both fell. This research ought to be replicated in NYC to better understand the effects locally. If the research came to the same conclusions in NYC as it did in San Francisco, it could spur on more development. 45% of the housing stock in NYC is subject to rent controls. With that in mind, if the research were replicated here and arrived at the same results it might do wonders to put local pols at ease.

The other important thing to note is the concept of moving chains. The moving chain refers to the idea that higher earning people move “up the chain” into more luxury, amenity-rich buildings, thus leaving open their former apartments for those people coming from lower income areas. Further, those higher earners who become the first occupants of the luxury properties will eventually leave these new developments. According to W.E. Upjohn Institute for Employment Research, when this cycle gets repeated enough times, then “Of all the tenants moving into the sixth apartment in these chains, 40% were from low-income census tracts.” That is to say, even luxury housing built today could over time become something closer to work-force housing and house many residents from lower incomes, or from lower income census tracts. And this idea makes sense intuitively. Over time that luxury building maybe isn’t so luxury. Sort of like getting a hand me down shirt from your older brother growing up. Still, getting that hand-me down shirt is great. And if this concept is really happening at scale, then that weakens the notion that displacement necessarily follows from new construction.

Sources: Wall Street Journal, Bloomberg