Condo Conversions in NYC and Capital Revival: Hochul’s Housing Play

Hochul amended the threshold for multifamily-to-condominium (condo) conversions, lowering the tenant approval requirement from 51% to 15% on Friday. This will have monumental impacts on the multifamily industry, and those who read my newsletter will be clued in before everyone else.

Please note that this is a longer article - scroll to the end for the findings or call me for the full details.

Lowering the Bar for Condo Conversions

In a move that rewinds a key 2019 Housing Stability and Protection Act (HSTPA) reform, New York’s new Affordable Housing Retention Act (AHRA, S1354) slashes the tenant approval threshold for converting rental buildings into condominiums, from a 51% majority of residents down to just 15% of bona fide purchasers (i.e., legitimate, arm’s-length buyers who are not related to the owner or sponsor). In a significant departure from the requirements that emerged from 2019's HSTPA, purchasers do not need to be existing tenants; they simply need to move in when occupied apartments become vacant. This means a landlord no longer needs over half their tenants on board to convert a qualifying building.

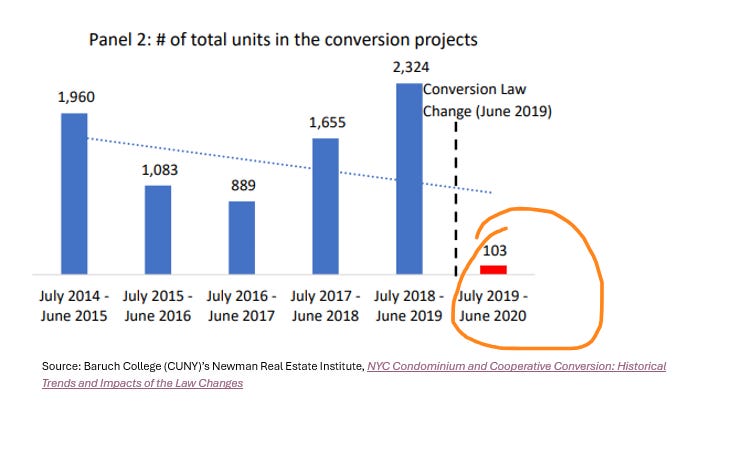

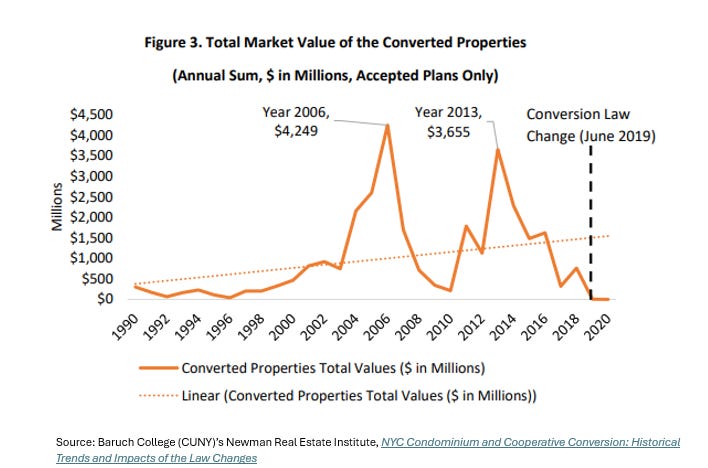

Since the HSTPA was passed in 2019 and applied the 51% majority requirement, very few apartments have been converted into condos. Conversions nearly came to a halt, as evidenced by research from Baruch College (CUNY)'s Newman Real Estate Institute, shown below. By dialing down the requirement, Governor Hochul is reopening the condo conversion pipeline, albeit with some critical new strings attached.

Under S1354, owners of certain rental buildings in NYC can convert apartments to condos in exchange for agreeing to either preserve expiring affordable units, or to expand the number of such units within the property. This isn’t a green light for unchecked deregulation. It’s a deal where owners can have more freedom to cash out via condo sales in return for shoring up affordable housing in their properties. In negotiating this policy, Hochul has put condo conversion opportunities back on the table.

A Niche Group of Eligible Buildings

Not every landlord can rush to take advantage of this rule. By design, S1354 targets a limited subset of buildings, resembling more of a surgical strike than a citywide sweep. Only mixed-income multifamily buildings in New York City, built after 1996 and containing 100 or more units, are eligible. That means the law is aimed squarely at the generation of buildings financed in the late 1990s and early 2000s with affordable housing incentives (think of the 80/20 developments that used tax-exempt bonds or the 421-a tax abatement). Many of these properties have a chunk of rent-restricted apartments set to lose their affordability soon as regulatory agreements expire. Without intervention, those subsidized units could flip to market rate, displacing lower-income families (think 421-a properties). S1354 provides a new path and allows the property owner to convert apartments to condos (capturing significant value), if and only if they extend or expand the affordable component. By limiting eligibility, the law focuses on projects where units might be at risk of falling into disrepair without an infusion of capital. Growing the velocity and volume of condo conversions can provide that capital.

Notably, 421-a properties from the late 1990s that received tax breaks for keeping apartments beneath specific Area Median Income (AMI) levels and/or under rent stabilization should be good candidates for this new program. In exchange for keeping certain designated income-restricted units affordable into perpetuity, owners are granted the ability to sell other units as condos and make profits. The idea is that this profit can be used to better maintain distressed buildings headed toward disrepair.

How the New Conversion Process Works

For owners of a qualifying building, converting rental units to condos will not be as simple as filing an offering plan and popping champagne. S1354 builds in a rigorous application and oversight process to ensure public affordability benefits are delivered. Before anything else, landlords must secure approvals from housing agencies that their building(s) is(are) eligible and will meet all affordability preservation criteria. Then, they must set aside the (additional) apartments that will be rent-restricted. Finally, owners must prepare preservation plans for approval by housing officials and the Attorney General (AG). This plan outlines how owners will “commit to the stewardship of permanently affordable units,” in addition to all the standard items in condo conversions, such as obtaining AG approval on offering plans.

Beyond these steps, owners must also establish reserve funds for building-wide improvements and dedicated capital funds for affordable units’ upkeep. This is a nod to the concern that some affordable units in these buildings need serious repairs. The preservation plan likely will detail how much money is set aside to rehabilitate and maintain those low-income units so they don’t become second-class apartments in the new condo. Also, to limit the business plan of selling just 15% of condo units and then skirting rent stabilization law by keeping the remaining units as rental apartments, the policy requires sponsors to sell at least 51% of the units within 5 years of the condo’s formation.

The Lure for Investors and Landlords

The reward for contending with all these regulations and requirements is that owners get to capture back some of the value locked in their buildings. The idea is simple: New York City condos typically carry far higher price tags (per square foot) than equivalent rental buildings, especially if units in those buildings were under any regulations. By converting, an owner can escape the limits of rent stabilization and monetize apartments at full market value.

What does that look like?

Consider that a 700 square foot two-bedroom rent-stabilized unit in Manhattan might rent for $2,000 a month due to years of low permitted increases. Let's assume the unit's carrying costs are $1,000/month, so the net income of the apartment is just $1,000 per month. At a 7.0% capitalization rate, that unit's value as a rental apartment is about $170,000. However, that same unit might sell for $1 million or more as a condominium, depending on the neighborhood's going rates. Of course, the costs to reposition and refurbish the apartments have to be considered, and these will often exceed six figures if they are to be prepared with condo finishes. But the spread between renovation costs and sale price should well exceed the profits that come from selling at $170,000 per unit.

In 2023, the median condo price on the Upper West Side was about $1.55 million, according to Miller Samuels, and the average price per foot was $1,969. On the Upper East Side, median condo prices for a 1-bedroom were around $855,000, and 2-bedrooms around $1.9 million, with averages of about $1,270–$1,700 per square foot. These values dwarf what a rent-regulated landlord could obtain on a price per unit by selling the building as a single rental property. S1354 gives landlords some opportunities to capture those condo-level prices and take their units out of warehoused status.

The warehousing of apartments is directly tied to HSTPA and how it has sharply limited the ability for investors to recoup renovation costs. Today, owners can spend a maximum of $15,000 on an apartment upgrade (Individual Apartment Improvement) and raise the rent by only about $89 a month. Even after recent tweaks (the cap was raised to $30k–$50k), the allowable rent bumps ($178–$347) are often too meager to justify major capital outlays. The low returns the government currently offers to improve many older units has contributed to the glut of dilapidated, empty apartments that weren’t worth refurbishing under rent limits. Condo conversions flip that calculus. Now, investing in unit upgrades can significantly increase an apartment’s sale price, yielding a real return. For instance, investing $50,000 into the renovation of a worn-out kitchen and bathroom might barely move the needle on rent, but it could easily boost a condo’s sale value by several times that (imagine turning a $300,000 unit into a $400,000 unit). For an entire apartment, an owner might spend approximately $500,000 on capital improvements and see roughly $800,000 (or more) in added value across the condos sold. That’s a compelling ROI that simply isn’t attainable under long-term rent stabilization. And this profit can stave off buildings falling into disrepair and will encourage warehoused units to be used once more.

Hurdles and Market Realities

Before we assume every eligible landlord will jump on this, it’s important to note the challenges involved. First, the regulatory gauntlet is real. Coordinating approvals between multiple agencies like HPD, HCR, DOF and the Attorney General’s office means conversions won’t happen overnight. Crafting a credible preservation plan (including a long-term affordability agreement, physical renovation scope, financing plan, etc.) is a complex task. There could be multi-agency delays if, say, the city’s Department of Housing Preservation & Development (HPD) and the state’s Division of Housing and Community Renewal (HCR) each had to independently offer comments and feedback on preservation plans.

Besides regulatory concerns, there is also market risk. Selling condos, especially in buildings that weren't originally built as luxury condos, can be challenging. Local real estate conditions will heavily influence whether a conversion makes financial sense. For instance, in Manhattan's Upper West Side and Upper East Side, pricing and demand for condos are robust. As noted, 1- and 2-bedroom condos in those areas often fetch around $1.55 million+ and $1.8+ million, respectively. However, condo sales might be less appealing in neighborhoods further away from Manhattan's core and that are more working-class.

In Upper Manhattan neighborhoods, including Washington Heights and Inwood, the numbers for condo conversions are a little harder to calculate. In Washington Heights, the median sale price for co-ops/condos in 2023 was around $478,000, with an average of about $582 per square foot. In Inwood, median prices were even lower, at roughly $399,000 in 2023, averaging about $620 per sq. ft. And if we venture to the Bronx, where the condo market is thin, the median Bronx condo sold for only about $289,000 as of 2024. Buyers will purchase buildings in these neighborhoods at price that come out to just $65,000 - $100,000 per unit. The 3-bedroom in Inwood can sell for more if packaged as a condo. But, will the profit margin be enough? After sponsors pay for renovations, transfer some units to a nonprofit, and cover transaction costs, there isn't much profit margin left. If the projected sell-out value isn't high enough, the owner could lose money trying to convert. Additionally, owners must weigh whether selling 80% of the apartments as condos yields more value than keeping 100% as rentals. In many cases, it will – but not universally.

Today’s market conditions also feature higher interest rates and an uncertain economy, which can impact condo sales. Further, property owners don’t make one big sale like with a rental property. Instead, they sell unit by unit, and that can sometimes take years. During the sell-down period, they must service any debt and also operate any units that remain rentals (now under stricter rules because of the conversion). S1354’s requirement that sponsors sell 51% within 5 years adds pressure – they can’t just test the waters indefinitely. If the market is soft (say, few buyers for million-dollar apartments in a fringe location), an owner could be stuck in limbo, having converted but unable to fully cash out.

Still, in spite of these hurdles, many owners will likely attempt it because the upside is so significant in the right market. We might see an initial wave of conversions in neighborhoods like the Upper West Side, Upper East Side, and Downtown Brooklyn, where condo comps are strong, and fewer in, say, Inwood or the Bronx, unless there's a unique circumstance.

Nonprofit Partners and Affordable Units: A New Dance

One of the most novel aspects of this law is effectively making a nonprofit co-owner of the building and a stakeholder in its future. When a conversion happens under S1354, the affordable units don't just vanish or turn into market-rate condos – they must be preserved under a nonprofit's stewardship. This approach ensures the permanently affordable units remain affordable (likely with renewed regulatory agreements and subsidies). It’s a clever structure, but it also introduces complexity in execution.

For one, the owner needs to find a willing and able nonprofit (or community land trust) to take on those units. Nonprofits will scrutinize the deal to make sure they can maintain those apartments financially. Typically, the units would either remain rentals (with the nonprofit acting as landlord) or be converted into limited-equity co-ops/condos that low-income tenants can buy. The legislation allows the affordable units to convert to affordable homeownership units with agency approval. So, a nonprofit might later sell those units to qualified buyers at restricted prices, creating homeownership opportunities for low-income families. In any case, those units will not sell for anywhere near market value, by design.

From the original owner’s perspective, this is essentially a giveaway of part of the building’s value. They might receive a nominal sum for the affordable units (or nothing at all) – the law doesn’t promise any payment, just the privilege of doing the condo plan. Economically, the owner is foregoing whatever the value of those affordable apartments would be if rented or sold freely. That’s the equity contribution they make to the joint venture with the government/nonprofit. In return, they hopefully supercharge the value of the remaining units.

However, coordinating this transfer is tricky. The offering plan will need to delineate which units are affordable and being conveyed to the nonprofit (or retained as such). The condo declaration might be structured so that all affordable units are grouped into one condo parcel owned by the nonprofit or a series of units owned by the nonprofit. Either way, the new condo's governance will involve both individual unit owners and a nonprofit owner. This could raise questions: How are common charges split? (Presumably, the nonprofit will pay its share for the units it owns, funded by rents or subsidies.) Will the condo board have representation from the nonprofit? (Likely yes, based on its unit ownership.) All parties will need to cooperate to make the building run smoothly, since a condo with a mix of market and low-income units is a bit of a social experiment. It's not unheard of – some inclusionary housing condos already have such setups – but it requires coordination.

For investors, partnering with a nonprofit might be new terrain. Some owners could balk at sharing their property. But others will recognize that without this arrangement, they can't unlock the condo upside. Organizations like Habitat for Humanity or local community land trusts are supportive of this program – they see it as a chance to take stewardship of the affordable units and ensure those homes are preserved. If done right, it's a win-win: the investor gets to monetize its value, the nonprofit expands its affordable housing portfolio, and tenants get stable, improved affordable homes.

In Closing

This new policy is essential to understand and contend with because it is now a reality. Unlike other policies that are still prospective that I have discussed recently, the AHRA (S1354) is to be included in the state budget and will pass into law shortly. More details will emerge in the coming weeks that detail more information on how the policy roll-out will look, and in my view, all multifamily owners with post-1960s buildings should review this bill. Time will tell what adoption looks like, but the details of the bill are here, and you should get familiar with them. Nixon Peabody created a great summary of the new law here.

The return on investment for capital expenditures on rental apartments has been dismal since the HSTPA. For the right building owners, condo conversions offer an exit ramp – a "pressure valve" that can unlock value and cash flow, stabilize distressed assets, instead of trying to squeeze blood from the stone of regulated rents.

For those who qualify, the time to act is now. Reach out to your legal team to assess your properties' eligibility and begin outreach to brokers, housing agencies, and non-profits to consider feasibility studies for your properties.

I am bullish on NYC Multifamily

Best Regards,

Romain Sinclair

646 326 2220

Sources

New York State Assembly. (2025). S1354: Affordable Housing Retention Act - Assembly Bill Summary. Retrieved from https://assembly.state.ny.us/leg/?Actions=Y&Committee%26nbspVotes=Y&Floor%26nbspVotes=Y&Summary=Y&Text=Y&bn=S01354

Hochul, K. (2025). Governor Hochul signs legislation to make housing more affordable and accessible. Office of the Governor. Retrieved from https://www.governor.ny.gov/news/governor-hochul-signs-legislation-make-housing-more-affordable-and-accessible-part-fy-2026

Nixon Peabody. (2025). Affordable housing retention act's impact on condo conversions and affordable housing preservation. Retrieved from https://www.nixonpeabody.com/insights/alerts/2025/05/08/new-york-introduces-the-affordable-housing-retention-act

Baruch College Zicklin School of Business. (2021, May 5). NYC condominium and cooperative conversion: Impact of the recent law change. https://zicklin.baruch.cuny.edu/wp-content/uploads/sites/10/2021/05/5.5.2021_NYC-Condo-Conversion_Impact-of-the-Recent-Law-Change_May-5th-2021.pdf

Miller Samuel Real Estate Appraisers & Consultants. (2024, January). Elliman Report: Manhattan Decade 2014–2023. https://millersamuel.com/files/2024/01/Manhattan-10YR-2023.pdf