Deal Story - 12 Rent Stabilized Units Sold for a Good Price?

Editor’s Note:

I am happy to announce that I have left my post at Greysteel and recently joined the NYC-focused CRE brokerage firm Terra CRG.

Happy Holidays!

926 Hart Street and 80 St. Nicholas Avenue are two six-unit residential walk-up buildings that were sold in the Summer of 2023. Basic details of the deals are below.

Using a combination of in-place rents and below-market, pro forma rents on four vacant apartments, the purchaser is going into a deal that stabilizes at a high seven capitalization rate more or less immediately. The apartments that need to be leased contain minimal lease-up risk. The blended gross rent per square foot when the new rents are added into the rent roll barely reaches $26. The rent per square foot on well-renovated, 1910-1920s vintage buildings, "comparable buildings," is in the mid $40s per square foot, or 70% higher than these buildings. On the very high end, with exceptional renovations and high bedroom counts (like you would expect to have in 80 St. Nicholas, a corner building), you would expect gross rents to reach north of $50 per gross square foot. That means the path to the upside here is swift because it will be a no-brainer for renters to pick these buildings to live in versus others.

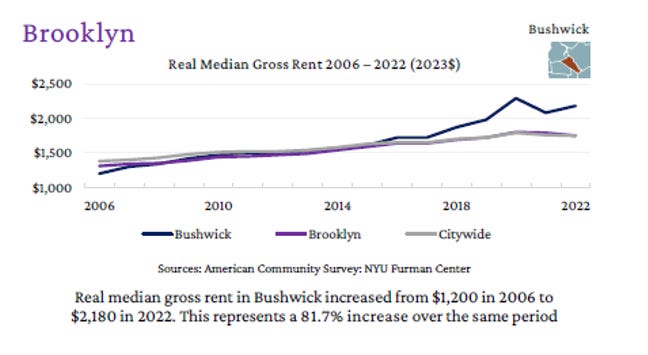

There is a rather large wedge between renovated building rents and these buildings' rents because these properties fall under the umbrella of rent stabilization. The rents in Bushwick for fair market apartments have taken off since 2008. Even though the market has slowed since then, the spread between Class C apartments and Class A rents can be as high as 100%, and that does not include new construction or elevator properties with amenity packages.

Bushwick, where these properties are located, saw significant rent growth in the last two decades.

Light Value-Add

The common areas, the basements, and the apartments were all in good condition which suggested minimal cap-ex requirements on Day 1 after closing. Further, there were almost zero DOB or HPD violations at the time of sale, which was remarkable for a rent stabilized building. But okay, fine. Let's add $150,000 to the transaction to cover initial capex (whether used or in reserves) and $50,000 in closing costs (let's assume there is no CEMA here). With NOI of ~$180k and a project cost of $2.5m in year 1, the new purchaser would forecast a yield-on-cost of 7.23%. No matter where you like to hang out on the risk/return curve, you must appreciate the ease of the business plan here. No HVAC upgrades, no plumbing, no roof to be redone. And the units will all but lease themselves because of their price point.

The Problem

The problem is that it's rent stabilized, you might say. Or, that it's too small. Or that it's too… Yes, there are problems with this deal just like with any deal. At the time being, the new buyers cannot alter the size/shape of the buildings. Similarly, the buyers cannot strike down the rent regulations governing the apartments. But, they can choose to purchase buildings that soften the blow of rent stabilization.

The main concern with rent stabilized assets is the twin issue that rents cannot go up while, at the same time, expenses are uncapped. Some owners have looked in dismay as 50% increases in insurance premiums have dwarfed modest rent increases granted by the Rent Guidelines Board. Even more universal than insurance price increases owners have faced is the heavy burden of property tax growth. Though your rents cannot grow, NYC's budget grew more than 5% from $107bn last year to $112bn in 2025. That means property taxes will likely go up at similar rates to keep up and fund the city.

Except with small buildings under 10 units. If you buy buildings with fewer than 10 apartments, you will be capping your rate of property tax growth to 8% a year, or an average of 6% over five years, as I covered here. This is what that looks like in practice.

Purchasing larger assets usually means obtaining cost savings by bringing management and third-party vendors in-house. Achieving scale also enables operators to negotiate for better rates/per unit with outsourced service providers. Vying for economies of scale is good business and is recommended. However, as the chart above illustrates, scaling doesn’t work with property taxes in NYC. Property taxes paid per unit do not get cheaper as more units are in the building. My highly anecdotal data of small and large buildings in Bushwick suggests that larger buildings pay almost 60% more in property taxes per unit than smaller ones with tax class protections. While this exact number may not hold, the direction of traffic is correct. Larger Buildings, defined as having more than 10 apartments, have higher property tax burdens to carry.

This wouldn't matter if property taxes were only a nominal portion of operating expenses. But that's far from the case. Property taxes in some buildings can make up 60-80% of operating expenses before debt service. When the largest expense by far in your investment doesn't flatten out when you scale up your number of units, it doesn't matter if your other costs shrink some. The Pareto principle comes to mind here. According to the principle, 80% of the consequences come from 20% of input. Though property taxes may be represented as just one line item, it makes up the lion's share of operating expenses.

If investors pay attention to tax-protected properties, it may allow them to buy rent stabilized property more efficiently and comfortably. Because property taxes are such a large part of operating expenses, when investors remark that expenses are going up more quickly than rents in RS properties, they are really referring to property taxes. Buying smaller property may offer a way out of the logjam. Though repositioning rent regulated buildings and creating value right away is not possible, it is possible to purchase these assets if pricing adjusts closer to an 8-9% yield on cost.

Do you agree or disagree? Would you have bought this deal?

Pictures of vacant apartments

If you are curious about this past sale, please reach out. I have full income and expenses, DHCR, expense receipts, and more.

I am bullish on NYC Multifamily.

Call me at 646 326 2220

Best Regards,

Romain Sinclair