Does Good Cause Eviction increase the probability of bank runs?

Hopefully a perspective related to Signature Bank that you have NOT yet thought about

Recap

Signature Bank clients rapidly withdrew their funds on Friday March 10th with concerns over the bank’s liquidity. Over that weekend, the bank scrambled to get emergency funding to support its withdrawals but was unable to. As a result, New York regulators took over the bank and removed the executive team. You’ve seen this explained before. There are more flavorful and meaty accounts here.

New York Community Bank (NYCB)’s subsidiary struck a deal with the FDIC to buy a portion of the Signature bank business. NYCB would buy $34Bn of customer deposits and $12.9Bn of Signature loans for $2.9Bn. This trade comes at close to no premium to asset value, according to Chris Whelan, Chairman at Whalen Global Advisors, which means a great deal for NYCB, an experienced commercial real estate (CRE) lender in NYC. Interestingly, none of the loans bought by NYCB would be CRE loans. The deal mostly consisted of business loans to healthcare companies.

Why didn’t NYCB buy the real estate loan portfolio?

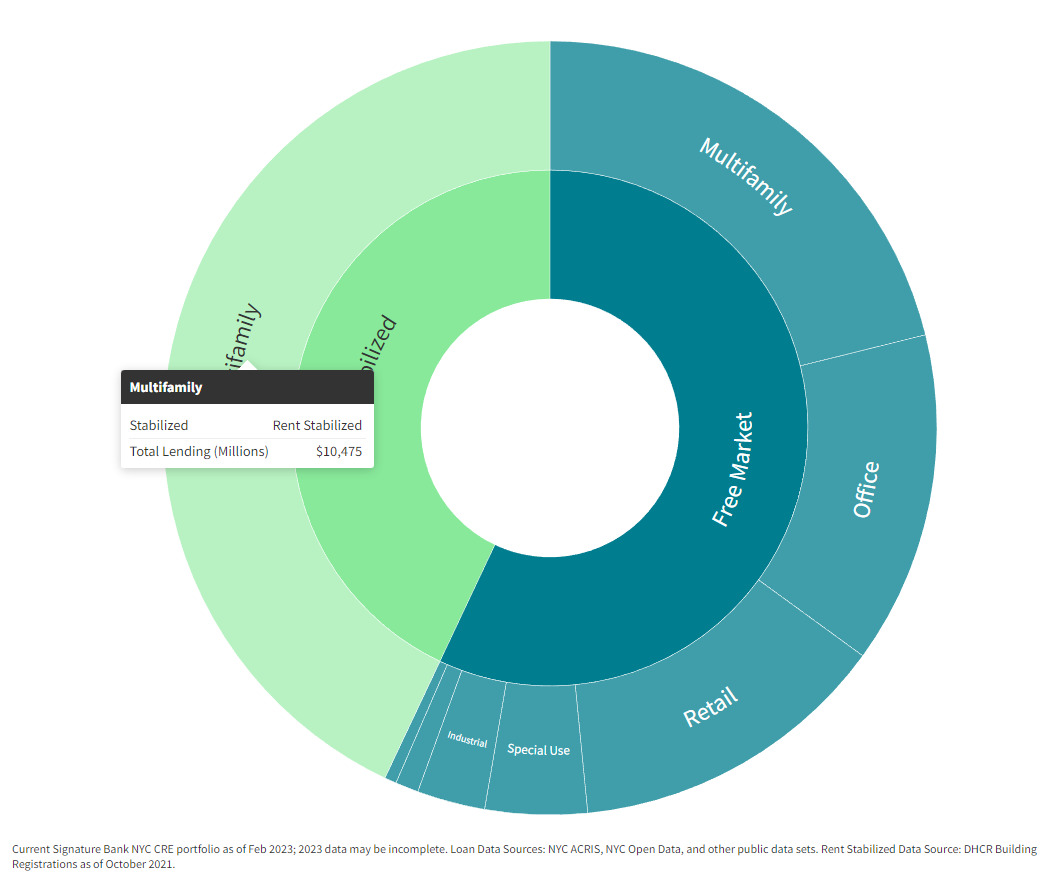

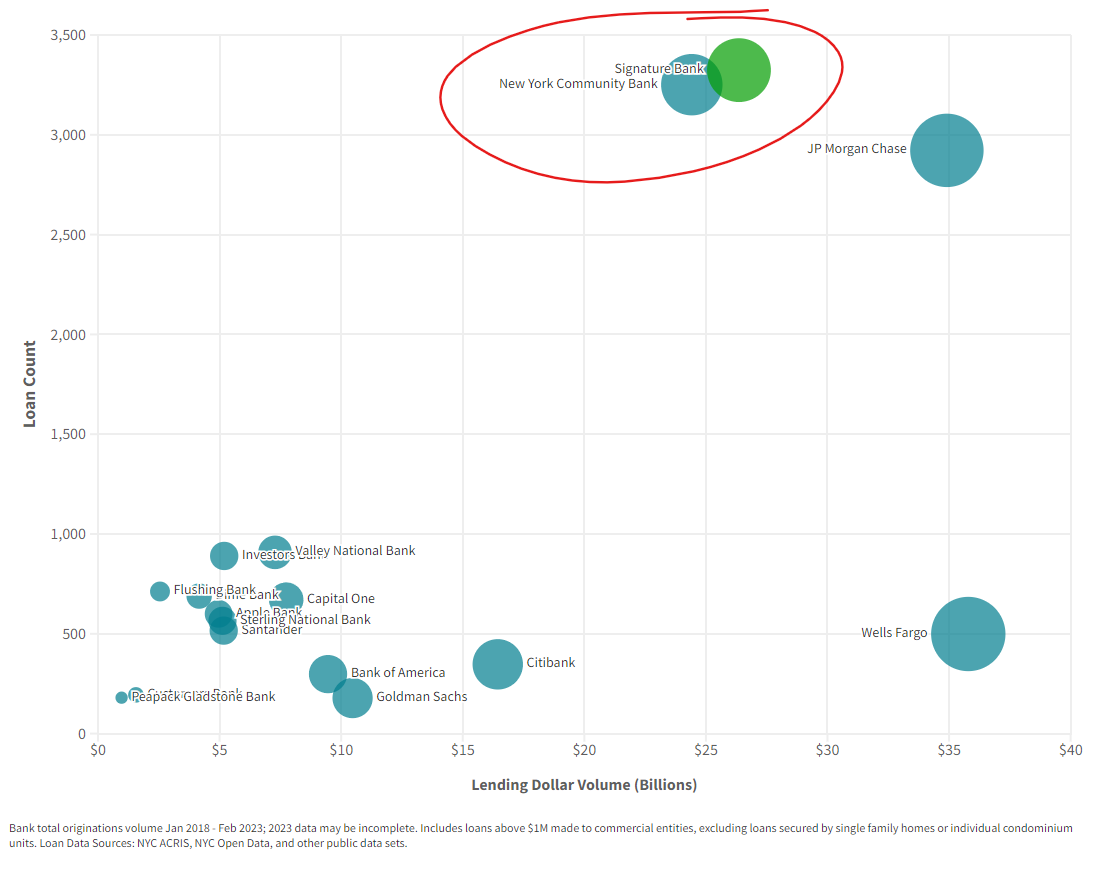

Lots of talk in news columns (here and here) point to fears of taking on rent stabilized multifamily loans. According to Maverick, a real estate investment firm, Signature Bank originated the greatest number of commercial mortgages in NYC from 2018-2023 and came only after Wells Fargo and JP Morgan Chase in loan volume during the same period. Signature held approximately $10.5Bn of rent stabilized multifamily debt, and $5.1Bn of multifamily free market debt.

Signature Bank’s CRE loan portfolio

Maybe NYCB didn’t buy the real estate loans for the same reason that they didn’t buy Signature’s crypto business: its leaders were afraid of a worthless asset. Maybe rent stabilized loans have just totally collapsed in value. Maybe, the estimated 20-45% reduction in property values from 2019’s rent laws are now starting to be realized and are stifling refinancing needs. Maybe the chickens are finally coming home to roost and, in the words of broker/owner Lazer Sternhell, “It’s all over.”

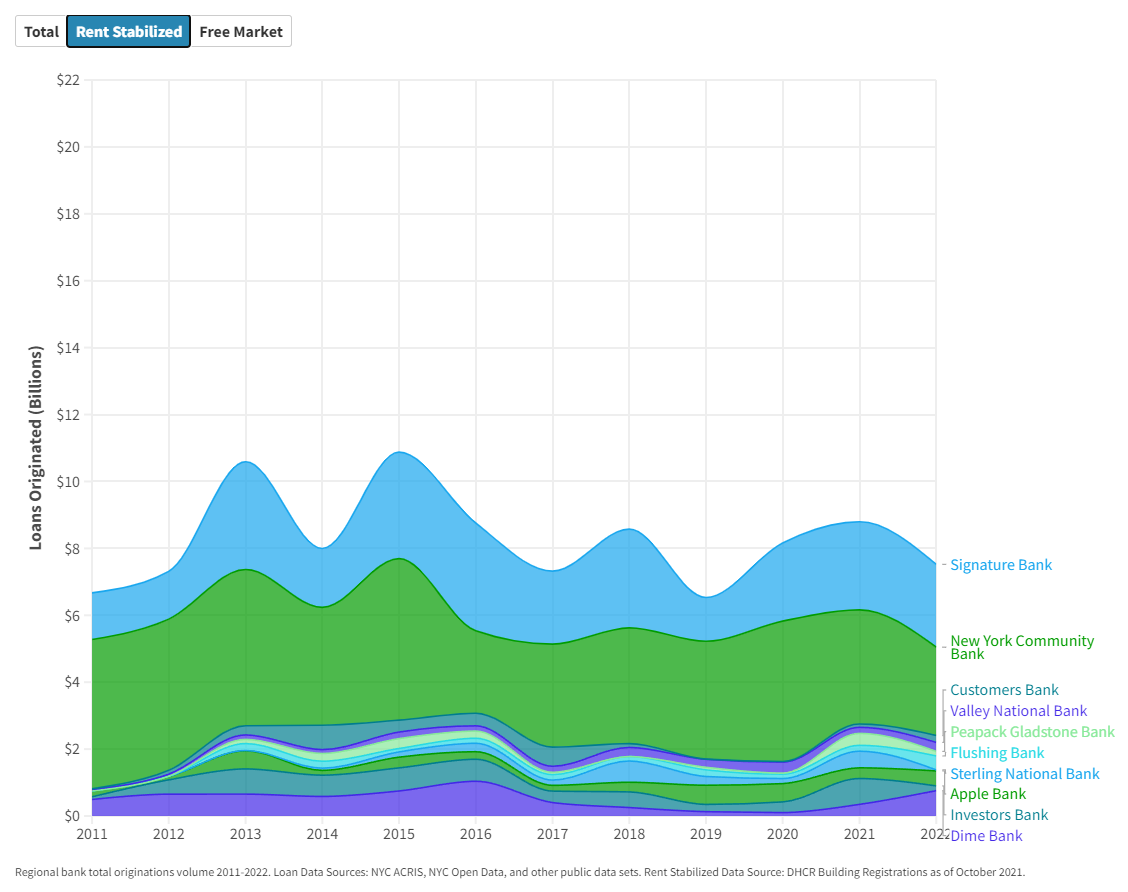

But, then again, NYCB is right behind Signature Bank in terms of lending volume and number of loans originated. Many of NYCB’s loans are rent stabilized too, and it’s doing fine.

CRE loans originated in NYC by count & volume: 18’-23’

Volume of RS loans originated in NYC: 11’-22’

According to an NYCB spokesperson, NYCB leadership was interested in diversifying their existing business portfolio. This is believable. It’s not like NYCB carved out the $10Bn of rent stabilized multifamily loans from Signature’s $35Bn debt portfolio and bought the rest of the loans. They didn’t take on any of the multifamily loans. I’m not saying that RS debt is appealing over free market multifamily debt, but it is interesting to see how quickly Signature’s loans are being labeled as “toxic waste” or, “grow[ing] hair on them”, because they haven’t been purchased yet. Now consider if all loans on New York multifamily properties with >4 residential units became subject to rent caps, or de facto rent stabilization. All the concerns over Signature Bank’s debt could spill over into all other community banks, which are estimated to hold ~70% (or 80% according to TREPP) of all commercial real estate loans in the U.S.

I am not concerned with the sale of Signature’s CRE loans, but I am worried about what happens to free market multifamily loans if Good Cause Eviction passes in New York. There are plenty of investors bullish on the long-term prospect of NY rent regulations softening. They are in the minority to be sure, but those contrarian investors exist, and I have sold buildings to them. Still, valuations for rent stabilized buildings are lower than free market buildings because they present less of an opportunity to raise rents in the future. That means a loan backed by a free market property rather than a rent stabilized one, all things held constant, has a higher probability of being repaid. That means those loans are worth more to an investor and rent stabilized loans are worth less. If Good Cause Eviction happens in the form currently being mulled over, then all buildings in NY become rent regulated and all the multifamily loans lose value. This has massive consequences and implications for lenders and borrowers in a normal market. But today, there is also the risk of bank runs and flighty deposits. I believe that Good Cause Eviction could lower loan values and increase the risk of bank runs. That would be tragic.

Just how close are we to that happening?

The NY Senate, State Assembly, and Governor are embroiled in negotiations over the state budget and the senators / assemblymen are making it clear that they are willing to pass Good Cause Eviction, effectively making all properties in NY State subject to rent stabilization. Lawmakers seem supportive of Governor Hochul’s Housing Compact plan, which would add 800,000 units to NY state in the next 10 years, but it looks like they want to create legislation for Good Cause Eviction and Housing Voucher programs. It’s tough to say how this will go. We will find out in a few days what the final budget will include. Stay tuned!

Here are some reasons to remain optimistic about where we are today re-regional banks:

The Federal Reserve is offering credit lines to banks to borrow funds at overnight funds rate, as long as they post collateral. This will quell many fears about deposits being lost.

The loans in NY are solid. For instance, only about 0.42% of Signature Bank’s multifamily loans were past due.

It’s hard to know exactly what will happen next. Right now, it seems like the Globally Systemic banks are a safe bet, and depositors have been taking their deposits there. Credit may be tightening at some community banks, as they seek to shore up their deposits and play defense in a volatile environment. That said, the spigot has not closed and community, regional, and national lenders are continuing the lend on multifamily and mixed-use projects in NYC. The current turmoil is tolerable. The most imminent threat to property valuations and lenders is if Good Cause passes.

Sources: Maverick, Wall Street Journal, The Real Deal