Full Analysis: The Looming Risks of Property Insurance Staring Us In The Face

Continuation From Last Week: Deep Dive Into the Twin Risks of Climate Disaster & Poor Property Insurance Strategy

TL;DR - Consider Investing in these kinds of stocks when **** hits the fan

The 2008 subprime mortgage crisis that culminated in one of the worst economic depressions in U.S. history was long in the making yet ignored by many in the know. Today, the catalyst for America’s next financial meltdown might come from hurricanes in Florida, wildfires in California, or flash floods in Colorado. The increasing rate and magnitude of natural disasters in certain areas is driving us to the precipice of a real estate crisis, likely to contaminate the broader economy and require a national bailout of property owners and insurers.

Insurance and the Real Estate Economy

Homeownership and property investment are at the heart of the American economy, with an estimated 206 million homeowners. According to the U.S. Census Bureau, homes and rental properties are the two most valued assets on consumer balance sheets. The Federal Reserve Bank of St. Louis(FRED) values the owner-occupied housing market at $43 trillion. That's 15% larger than the Nasdaq market cap and rivals the size of the S&P 500 index.

Bloomberg estimates that about 40% ($17.2 trillion), or 83.3 million homeowners have paid off their mortgages, thereby having no mandatory insurance requirements. A recent study by the Insurance Information Institute and reinsurer giant Munich Re revealed that 12% (25 million homeowners) “went naked” and opted out of property insurance in 2023. In other words, 30% of U.S. homeowners without mortgages are uninsured. This exposure represents a potential $5.16 trillion in losses—an amount that continues to grow as insurance premiums increase and the “go nakeds” increase in number as the costs of insurance rise due to natural disasters.

Insurance Premiums and Natural Disasters Trends

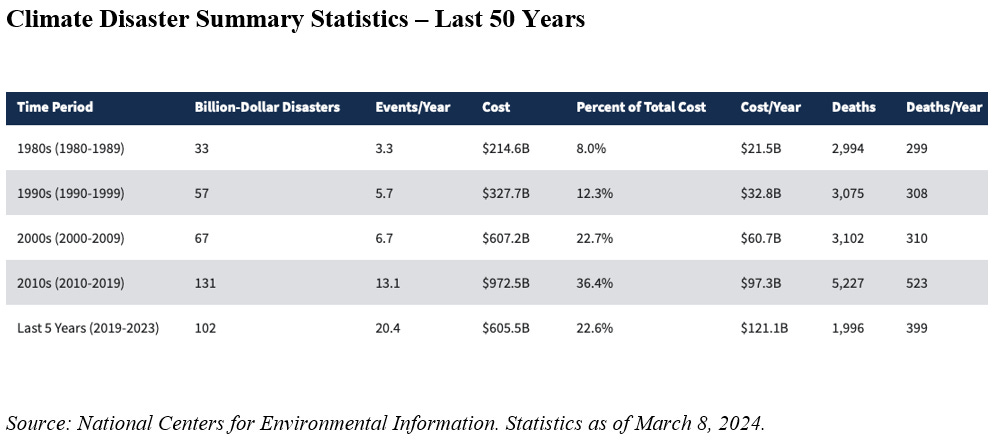

The National Oceanic and Atmospheric Administration’s (NOAA) National Centers for Environmental Information (NCEI) monitors and assesses the costs and impacts of natural disasters) to gauge future risks to life and property nationwide. NCEI’s data in Table 1 below shows the growth in frequency, magnitude, costs, and lives lost to natural disasters in America in the four decades since the 1980s.

The total cost of natural disasters per decade increased by 353%—from $214.6 billion during the 1980s to $972 billion during the 2010s. Correspondingly, costs per year per decade jumped from $21.5 billion in the 1980s to an average of about $60.3 billion during the 2010s. Deaths per year increased by 75%—from about 299 in the 1980s to 523 in the 2010s.

Billion-dollar disasters increased by almost 300%—from 33 in the 1980s to 131 in the 2010s, and the upward trend continues. The number of billion-dollar disasters in the 2010s nearly doubled that of the 2000s. In 2022 alone, there were eighteen $1 billion-plus natural disasters. Last year, the Maui, Hawaii, fire destroyed $3.2 billion in property value, and initial estimates put the March 2024 Texas panhandle fire, the second largest in U.S. history, in the $3 billion range. Also, the $121 billion cost/per year in the last four years between 2019 and 2023 is the highest on record and represents a 6-fold increase from the 1980s figures. If the trend holds between 2024 and 2029, the 2020s number will likely double that of the 2010s.

Besides the heavy damages they inflict on communities and the costs they levy on insurers, natural disasters pose a problem because they raise insurance costs for policyholders outside of impacted areas as well as inside those coverage areas. In the aftermath of the Texas panhandle fire, policyholders in Vermont who are renewing their insurance may find that their insurance premiums are increasing. When insurance carriers make a big payout somewhere, insurers must go elsewhere to try to plug the financial hole. Climate changes are driving the ballooning costs, volatility (frequency), and magnitude of natural disasters, and this has a pronounced effect on insurance costs.

The Looming Insurance Disaster

Significant shifts in the insurance landscape have proliferated since insurance costs have increased due to climate change. Where policy premiums rise precipitously in some communities, some homeowners without mortgages opt to “go naked” and go without insurance altogether. In other instances, insurance companies are entirely exiting markets because the costs of providing insurance coverage to communities are so significant and fraught with risk. These two responses can work together in a negative feedback loop. If fewer homeowners take on insurance, insurers must charge higher premiums to existing policyholders to balance their risks, leading to fewer insured homeowners. Conversely, the fewer insurers in the marketplace, the higher the premiums will typically be for policyholders, which could lead to fewer insured homeowners.

The exit of private insurers in many states and cities and the rising annual premiums have led to the rapid growth of state insurers of last resort. These state insurers are critical means for homeowners to insure their properties that private companies may deem un-insurable. Unless these state agencies know something that other insurance companies don’t and thereby have an advantage in underwriting insurance that competitors deem too risky, they are taking on more risk. On top of that, yearly premiums need to be low enough that the policyholder is willing to sign on. And therein lies the problem – what policyholders pay for insurance in many areas is not commensurate with the insurer’s expected value/cost of the property loss. By failing to share the risk with policyholders because that would lead to costly premiums, state insurers are absorbing a disproportionate share of the property risk. Over time, disproportionate insurance risk sharing will lead to disaster when turbulence hits the system.

It is difficult to overstate the importance of property insurance as a building block for the development of communities. Colorado State Representative Judy Amabile recently said, “There’ll be no real estate transactions, no businesses, hotels, stores” without affordable insurance, and “Insurance is pretty fundamental to keep things going.” Representative Amabile’s comments ring true because the real estate industry is driven by lending activity and lenders rely on insurance policies to protect their stake in assets before lending on them. Lenders won’t provide credit to markets without insurance, and real estate activity will dwindle. That will impact the private sector and the growth of public goods like schools, hospitals, and government properties. State insurers of last resort know this, which is why they sell otherwise uninsurable policies that effectively subsidize risks on paper, enabling the issuance of mortgages and allowing communities and economies to grow.

Each new climate disaster puts the economy and financial system closer and closer to the brink of crisis. Because of the insurance threat, U.S. Senator Sheldon Whitehouse, the Senate Budget Committee chairman, is leading an investigation into Florida’s insurance practice’s potential risks on the broader real estate market’s solvency. He said, “If Florida is the leading edge of the predicted crash in coastal property values, it could lead to an economic meltdown similar to 2008.” The climate disaster data, the rise in insurance costs, and the connectivity between real estate, lending, and insurance drive Whitehouse’s comments. As of 2022, vague estimates indicate a shortfall of approximately $1 trillion nationwide to cover property damage and replacement claims. The looming real estate disaster is just one large hurricane away from millions of “go-nakeds” losing their homes and state insurers of last resort defaulting on their replacement claims. Federal bailouts will be required when that happens, turning localized climate problems into fiscal crises.

California

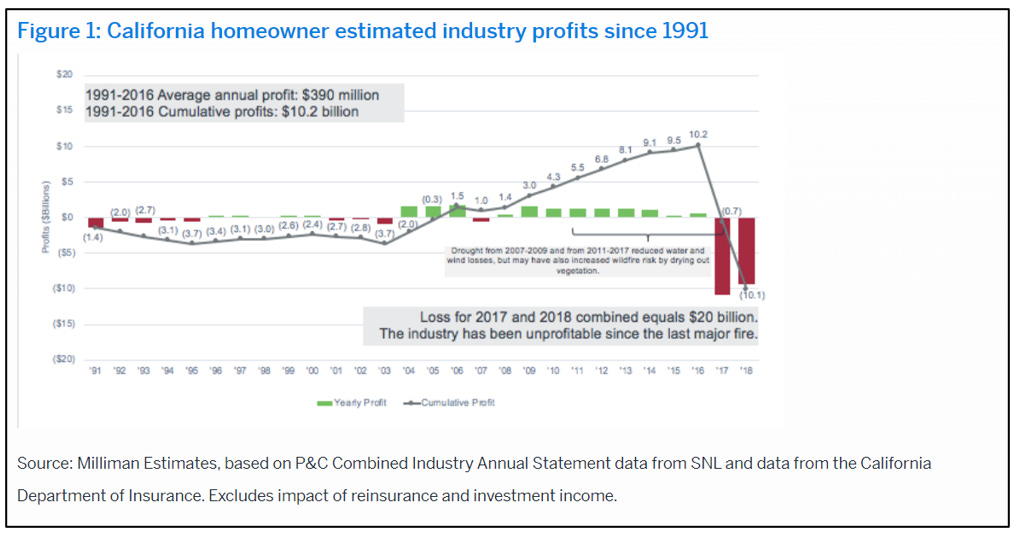

State responses to climate disasters and rising property insurance costs play an essential role in setting up the beginnings of the looming real estate crisis. In 1988, during a decade that saw 33 billion-dollar-plus disasters and $214 billion in total natural costs, California voters approved “Proposition 103,” which rolled back annual property insurance premiums and imposed state approval on future increases. The California Consumer Watchdog trumpets the $2.3 billion in homeowner savings from “Prop. 103,” from 2003-2023, and Milliman Research shows that insurance companies made close to $10 billion in profits from 1991-2016.

To classify Prop. 103 as a winning policy is incorrect. In the last decade (2010 - 2019), the United States had 131 billion-dollar-plus disasters and $972 billion in total natural disaster costs (297% and 353% increases, respectively, since Prop 103). Further, the 2018 California “Camp Fire” blazed for over two weeks, took at least 85 lives, destroyed over 19,000 buildings, and cost more than $16.5 billion. California had shockingly only earmarked $100 million of reserves to cover insurance damage claims. Celebrating Prop 103 undermines the potential billions of dollars in reserves required to cover expected claims by a single wildfire or other natural disaster.

California Homeowner Insurance Profits: 1991-2018

According to risk management company Milliman, the cost of wildfire damages for two years, 2017 and 2018, wiped out 25 years of underwriting profits for California’s private insurers. As a result of large claims paid by insurers and state-regulated price caps, large insurers like State Farm, USAA, Allstate, and others are reducing their coverage or exiting California’s insurance market altogether. The risks these private insurers refuse to underwrite are left to be absorbed by the state’s residual last-resort insurer.

Property Insurance Plans Service Office Inc., a research firm that tracks insurance programs, estimates that California’s state insurance program could now face a $290 billion shortfall, a six-fold increase since 2018. This growth rate will likely intensify, meaning the funding gap could exceed $1 trillion in a few years. With an estimated 11 million of its population living in high-risk wildfire zones and roughly 13% of homeowners opting out of insurance and going “naked” in 2021, California’s $9 trillion real estate market could be “ground zero for a sweeping financial crisis when the smoke clears” from another potential massive wildfire, according to Bloomberg Green.

Florida

Wildfires aside, Florida faces some of the nation's most significant climate-driven property risks. According to Universal Property & Casualty Insurance Company, 41% of all hurricanes that make landfall in the U.S. hit Florida. Further, Florida has twice as many hurricanes on average than Texas, the next biggest hurricane magnet in the United States. As a result of being ideally located for hurricane collision and the fact that the number of hurricanes and natural disasters is increasing, Florida home insurance has increased 33% each year since Covid, and that is pushing many residents to try and leave the Sunshine State, described in some publications as an insurance-fueled “exodus”.

As in California, private insurers are exiting Florida—more than a dozen in the last two years alone, expanding Citizens’ Property Insurance Company (“Citizens”) role as the state insurer of last resort. Citizens has almost tripled its number of insurance policies since 2018. Where California’s state insurer faces an estimated $290 billion shortfall, Florida’s Citizens has an exposure of $525 billion in potential losses—a level that has more than doubled since early 2022. If trends continue, Florida’s state insurer will have exposure to more than a trillion dollars of losses before 2023.

There are quick paths to insolvency in climate-risky places like Florida. According to a 2018 study by the University of Cambridge and Munich Re, if a Category 5 hurricane lands in Miami and the Florida coast, it could cause upwards of $1.35 trillion in damages. To cover this, Florida, where the average salary is $49,000, would have to assess $60,000 for every single person. That’s not feasible. Unless Florida's leaders do something to reform the insurance model, it is only a matter of time until the state's insurer defaults and Florida defaults and find itself in need of FEMA bailout assistance to prop up the real estate market.

After recent hurricanes, Federated National, which insured 140,000 Florida policyholders, went bankrupt and had to shut its doors, forcing it to cancel 56,000 plans after an insurance rating agency downgraded its financial standing. Bloomberg Green describes Florida’s situation as “a slow-motion insurance meltdown… as new people pour into the place with the greatest risk of flooding, a pattern playing out across the U.S.”

Florida is especially at risk from insurance company defaults because of the state’s dependence on property taxes. Florida has no state income tax and relies on real estate property values to fund its government via county property taxes. Broward County, home to Fort Lauderdale, received more than 20%, or $1.5 billion, of its budget revenues from property taxes. The next leading source of tax revenue is sales tax, which only contributed $117 million to the county. If a hurricane wallops the Florida coast and destroys enough homes, counties will lose significant portions of their income streams. On top of the destruction and distress, that will lead to reduced municipal services and severely constrain county and state operations.

Colorado

The problem with property insurance is demonstrated clearly in the state of Colorado. 2020’s Cal-Wood Fire racked up significant losses for insurance companies and sometimes drove tenfold insurance premium increases on properties. Insurance premiums have increased 50% on average because of damage from wildfires and hailstorms in Colorado between 2019 and 2022. In addition to and perhaps in response to the climate disasters, “76% of carrier groups shrank their property exposure in 2022 (through October),” according to a study by Oliver Wyman Actuarial Consulting (p.5 “Key Trends”).

Colorado responded to the rapid hikes in insurance premiums by adopting an insurance plan that includes creating a state insurer of last resort. According to the Oliver Wyman study, “A Residual Market Plan would provide a market of last resort that would allow high-risk homes to secure coverage,” where they otherwise would not be able to because too few insurance companies are left that would underwrite the property. Colorado is enacting a very similar policy to Florida, California, and the other states with state insurers of last resort. Colorado decided that the risk of costly insurance was too great. Significantly elevated insurance premiums would grow the share of uninsured homeowners, reduce tax income for counties and cities from slowing real estate activity, and invite community decline. Instead, lawmakers have opted to contend with the risk of a state insurer of last resort’s potential for default if a significant disaster strikes and the insurer is under budget.

Possible Solutions

As a nation, the U.S. could benefit from applying the urgency for solving terrorist threats in the last two decades towards solving climate disasters because failing to intervene could be deadly for the financial system. Solutions to the insurance problem should combine policy and market initiatives and involve education to change individual behaviors. Doing so may allow U.S. leaders to bridge seemingly intractable issues that pose risks to the local, state, and national economies.

To avoid national crises, state leaders must establish a better balance between keeping property insurance affordable and effectively pricing risks in climate disaster-prone areas. Today, insurance premiums are too expensive for homeowners and that is driving them to forego insurance. On the other hand, state insurers of last resort are underwriting risky policies that private insurance companies reject, and they are inadequately charging homeowners for the risk they are taking on. California’s Camp Fire in 2018 put this on display. The fire created $16.5 billion in damage, while the state only accounted for $100 million in reserves that year.

The Camp Fire brings to light another restriction present in the California insurance market but not exclusive to it. Carriers in California cannot price insurance policies based on expected future claims or from assessing other forms of disaster surcharges to fund the ballooning shortfalls. Disallowing pricing based on future risks keeps insurance rates low, but it sets up communities to fail by limiting the accurate allocating of reserves to cover natural disasters. It also discourages insurers from continuing their operations in the state because their prices & reserves are capped but their cost exposure is not.

Growing the insurance marketplace—both the supply and demand— will be a critical success factor in reducing insurance costs. Where the number of insurers is shrinking, risks and costs are climbing. When homeowners can opt out of insurance, they pass the risk on to others in the event of a disaster. Picture a raging fire, where negligence on the part of your neighbor can mean the fire more quickly goes from his house to your very own home and burns it down. Further, property insurance would be cheaper if all homeowners opted in, including those without mortgages. More homeowners signing up for insurance would allow insurers to spread the risks to more policyholders and lower rates. If more homeowners wanted insurance, it would encourage more insurance companies to enter the market. This would turn the current downward cycle of fewer insurance companies and fewer policyholders into a more upward, virtuous cycle that could expand coverage & reduce costs per home or unit. Building a premium into the property taxes of the uninsured or offering a discount for the insured would incentivize homeowners to obtain insurance and perhaps encourage the “go nakeds” to be clothed once more.

Another idea is to share the insurance cost burden with tenants and require them to pay renters insurance. Some NY insurance companies already require this for investment properties, and building owners in France and Western Europe similarly require it. Climate change is driving the jump in insurance costs, and landlords and homeowners are not solely to blame for the increase in climate events, so why should they pay all the costs?

Developing communal resiliency to the effects of climate change would also reduce insurance costs for homeowners. Defined by risk management professor Lee Bosher as “The sustained ability of a community to use available resources to respond to, withstand, and recover from adverse situations,” community resiliency defines the broad set of initiatives communities must undertake to be climate-ready. Updating building and zoning codes for new properties, as well as requiring the retrofitting of existing property to catch up to today’s climate risks, would lower insurance costs. There is also a concept here that says the whole is greater than the sum of its parts. Hypothetically, if all buildings in Jacksonville, Florida, have hurricane-proof building envelopes, the chances that storms damage or flood homes are far lower than if only most homes contain the protective materials. That lower risk factor will translate to deeper insurance savings because insurers will underwrite less risk for the entire community area.

In practice, achieving community resiliency means reforming the zoning and building codes to require more climate-resistant building materials to create structurally safer properties. Requiring coastal or forest homes to be water or fireproofed is one way of building communal resiliency. Another approach is to mandate that multifamily properties be retrofitted to be hurricane-, tornado-, and fire-proof. Much like the federal investments that have driven down the cost of solar panels and other renewable energy sources over the years, federal and state-led approaches to insurance subsidies should be created to incentivize better and defray the costs of strengthening existing and new properties.

States like California and Colorado might benefit from new zoning codes requiring vegetation-free buffer zones between property construction and woodlands. In places like Florida and other coastal areas with a high risk of flooding, elevation and reinforcement of property in flood zones, along with investment in modern infrastructure like battery-operated sump pumps and other technologies deployed in the aftermath of Hurricane Katrina, might also be viable options to look at. Collectively, these initiatives could do for property insurance what anti-theft devices have done for car insurance and could be monumental in stabilizing the property insurance market and reducing premiums while realistically managing risks.

Managing climate risks today will not only protect the built environment but also allow the U.S. to avoid the devastating effects that insurance company defaults would have on communities across the country and the global financial system. The orange haze that obscured Manhattan skylines in the summer of 2023 serves as a visual reminder that climate disaster trends are not stopping—evidence actually suggests that wildfire seasons are lengthening. A climate-driven insurance disaster happens when a wildfire causes damage greater than budgeted state reserves allow for, and suddenly, entire communities cannot secure insurance policies from carriers. When this happens, credit dries up, and communities will atrophy.

Though it’s impossible to control the tide of natural disasters, it’s well within our abilities to take an interdisciplinary approach to buttress the insurance system so that financial crisis is averted when (not if) disaster strikes.

Sources

Doug Bailey, “12 % of U.S. Homeowners Foregoing Home Insurance, Study Finds,” September 6, 2023, Insurance Newsnet.

Tim Brockett, Serena Garrahan, Mark Bove, Raghuveer Vinukollu, “The Weather Gauge – Driving Extreme Awareness and Resilience Forward,” Q2, 2023, Munich Re & Insurance Information Institute

Leslie Kaufman, Saijel Kishan and Nadia Lopez, “A Hidden Crisis in U.S. Housing,” March 5, 2024, Bloomberg.com