How Should Real Estate Investors Respond to Tariff-Induced Market Swings?

Last week’s big stock market dip was substantial - a 7.9% decline in Dow Jones Industrial Average, a 9.1% decline in the S&P 500 Index, and a whopping 10% drop in the Nasdaq. But the events of last week also serve as a reminder of why alternative assets are named so. Private alternative investments are less liquid, require more specialized knowledge to manage effectively, aren't governed by the same regulatory compliance framework, and most importantly, are not so correlated to the waxing and waning of the public markets.

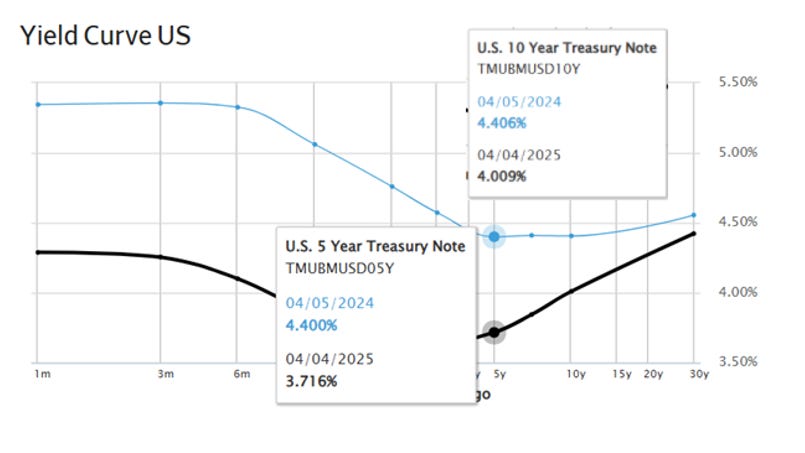

Real estate investments are a great example of alternative assets. Rents don't reprice overnight. Lease terms are often locked in. And most tenants don't change their space needs based on day-to-day headlines. To the landlord whose rent is owed next week or is signing a contract to sell his property, it doesn’t matter whether the average 401k lost tens of thousands of dollars last week. To the contrary, in response to the tariff announcements this week, some investors and brokers are beating their chests in affirmation of the now lower 5- and 10-year Treasury spreads. That’s an unusual reaction to a $2 trillion equity market wipeout. Or is it?

A few weeks ago, an investor I spoke to shared an agency quote with an interest rate of 160 basis points over the 5-year treasury yield, with full-term interest only on a five-year note, capped by a 1.35 DSCR on a conventional deal. That conversation happened before last week and the all-in rate was ~5.6%. In last week’s terms, and with the generous assumption that there is no widening of the index spread, that would translate to a rate and debt constant of 5.3%. This rate was achieved via a hefty point buy-down by the investor to make the deal work, and it certainly may not be available for all deals, but it is still remarkable (and yes, it is hypothetical, but I think it is on trend with the market).

The key question is whether the sharp jump in tariffs further lowers mortgage interest rates. What happened last week was:

The U.S imposed tariffs on the world (including China at 34%)

The U.S imposed tariffs onto Canadian automobiles of 25%

China applied a reciprocal tariff on the United States of 34%

What we should expect to see this week:

European tariffs on U.S. goods

Canadian tariffs on U.S. goods

Mexican tariffs on U.S. goods

The Market Moves Rates

In other words, more shocks are coming, more sectors will be impacted, and more charts will be down and to the right. As CBOE’s Volatility Index (VIX) indicates through its nearly 100% growth in the last week, investors are concerned about the volatility proliferating in the market. China's reciprocal tariffs hurt especially badly because the U.S. imports just under 15% of all its imported goods from China (feels like more), second and third only to Mexico and Canada. For this reason, reciprocal tariffs from China deeply hurt the American markets last week. In this vein, counter-tariffs from Mexico and Canada could prove even more costly, given the volume of trade between the U.S. and the two countries. Consumers and investors should also expect the European Union's response to hurt.

The Treasury Yield, which drives most fixed-rate borrowing interest rates in the U.S., doesn't wait for the Fed to chime in with its monetary policy actions to respond to macroeconomic shocks. Last week, investors rushed to purchase U.S. Treasury bills to try and sit out the anticipated loss in equity values. This big push drove up pricing for treasuries and tanked the yields, as investors were willing to accept lower yields for T-bills. This didn’t require the Fed to step in. Private investors simply moved their capital through the markets to reflect their economic outlooks. The markets also moved independently from the Fed when the 10-year treasury yield ended 2024 approximately ~110 basis points higher than before the announced rate cut on September 18, 2024.

Monetary Policy

The Federal Reserve's impact on the market could be significant. Though Powell says he will not respond to any remarks by President Trump, least of all cow to his demands to lower rates, Powell may have to lower interest rates out of necessity to fix the consequences of reciprocal tariffs if economic forecasts begin to spell inflation.

There are two ways consumers respond to these tariffs:

Inflationary: Prices on essential goods like food, cars, and utilities increase. Because demand for these items doesn’t change much across price levels, people keep buying them even as they get more expensive. Workers ask for higher wages as purchasing power declines, increasing business costs. Those rising costs then lead to further price increases. Some companies may respond by reducing output, which tightens supply and pushes prices up again. This is a typical cost-push inflation cycle.

Non-inflationary: Higher prices take hold and consumers start cutting back. They buy fewer goods, switch to cheaper alternatives, or stop spending on non-essentials. In response, producers scale back as demand falls. A new balance forms at lower levels of both supply and demand. In practice, the results will vary by sector. Some areas, like agriculture, may still see price increases, while others, like new cars, could see demand drop sharply since purchases can be delayed.

In response, there are three ways Chairman Powell could act:

Cut rates more than he originally planned for the year – although this runs the risk of bolstering consumer spending

Do nothing – this doesn't play well for the public and government officials, even if it's the correct move.

Raise rates to quell inflation

Each of these paths has its benefits and risks. In the next two weeks, I expect interest rates to continue declining due to international responses to tariffs, which could be fortuitous for real estate investment returns. If economic signals like new job reports, unemployment levels, and overall U.S. economic health start to show signs of an upcoming economic recession, Powell may lower rates with haste. Of course, he has to do this knowing that lowering rates could encourage businesses and consumers to borrow more money and consume more products and services, further heating the inflationary conditions, so there is a fine-tuning element there. Conversely, if inflation takes firm hold, Powell may be forced to pull the emergency brakes of the economy and raise interest rates.

Closing Views

Real estate investors should focus on deals and less on capital markets. Capital markets have always been unpredictable and that is especially the case now. Investors waiting for meaningful changes to the interest rate environment should continue waiting until the skies clear. Active players in the market doing deals before last week should keep doing so. The only exception is for those “extending and pretending” with one-year extensions on their loans, waiting to refinance until rates lower.

For those people, now is the time.

I am bullish on NYC multifamily.

Best Regards,

Romain Sinclair

646 326 2220

Subscribe as a paid subscriber for an exclusive event invitation below

Keep reading with a 7-day free trial

Subscribe to Romain Sinclair's NY Multifamily Newsletter to keep reading this post and get 7 days of free access to the full post archives.