IMPORTANT: Community Opportunity to Purchase Act

Community Opportunity to Purchase Act (COPA) appears close to passing in the New York City Council, and this is bad news for property owners and private actors involved in the purchase and sale of real property. In today’s letter, we’ll quickly recap what COPA is. We will also illustrate why the policy is problematic for the free flow of capital. Finally, we’ll address how the recent changes dramatically reduce the scope of application of the rule, allowing many owners to breath sighs of relief.

What is COPA?

If passed by City Council, COPA would require sellers of distresses residential property to give notice to Housing Preservation Development (HPD) of their intentions to sell. Alongside the notice requirement, the new rule would require sellers to submit detailed property and financial records to HPD to share with qualified not-for-profits. Key timelines to keep track off:

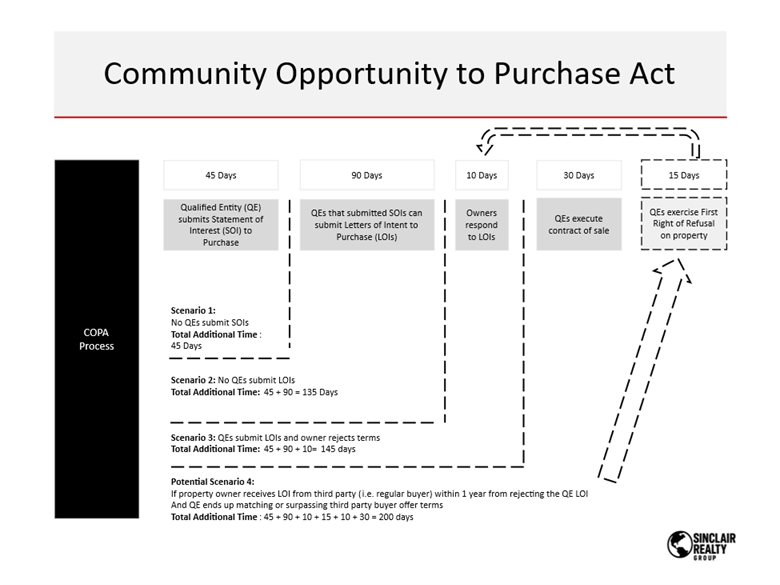

45-day initial notice period for “Qualified Entities,” which are comprised largely of not for profits to submit Statements of Interest (SOIs).

[If SOIs are received, then] 90-day period is accorded to QEs to submit formal Letters of Intent to Purchase (referred to as “bona fide offers” in the bill)

[If LOIs received, then] 10-day period for property owners to respond (accept/reject/counter).

The diagram below summarizes the timing and a few other clunky components like the first right of refusal that kicks in if property owners reject QE offers but instead entertain private market offers. During the periods laid out below, sellers of covered properties would not be able to enter contracts of sale.

Why is COPA Bad?

The public policy benefits from mandatory timelines are much harder to see than the red flags this raises for proper functioning of private markets. Here are a few cases:

1. Price Changes

As I wrote about in my June of 2023 memo about COPA, capital markets can completely transform over the course of 6 months and this can have acute impacts on asset pricing. The 10-year U.S. Treasury yield leaped from 1.8% in January 2022 to 3.05% in May 2022, effectively increasing costs of debt by around 15% (using a 225 basis point spread over Treasury). When debt costs go up so significantly, asset pricing recoils and value declines. Interest rate increases are one of several capital market changes that can occur from extended sale timelines. Other examples may include macroeconomic shocks such as global health pandemics, presidential elections, international conflicts, and stock market performance to name a few.

2. Idiosyncratic Buyers

a. The 1031 Exchange Buyer

Buyers in 1031 tax deferred exchanges sometimes pay higher prices for properties than average buyers. “1031 buyers” often have significant tax liabilities to incur if they do not purchase replacement properties. As such, they are heavily incentivized to buy properties, and sometimes paying above market price for property is still a better outcome than having to pay the relevant taxes. But better pricing comes with specific timelines. 1031 buyers have to close on replacement properties within 180 days from the closing of their sale, per the IRS. The introduction of COPA all but thwarts the reinvestment of capital into NYC multifamily from buyers looking to avoid capital gains taxes.

b. The End-of-Year Buyer

It is sometimes critical for investors buy or sell real estate in a given year, to support smart tax planning. Using tools like cost segregation, accelerated depreciation, and bonus depreciation investors can make large purchases to offset the taxes owed from a business or real estate sale that occurred in the same year. On the other hand, investors can cut loose a poor investment for a loss to offset income somewhere else. COPA and regulations like it add layers of complications for tax planning purposes. In today’s environment transactions are often subject to delays due to the unexpected. Adding a layer of regulation like COPA that mandates certain grace periods be extended to buyers could put sellers and buyers in precarious positions to accomplish their tax planning goals. And that is a big problem for capital flows into NYC.

c. Investment Funds

Investment funds typically have mandates that require investor capital be deployed by a certain date after it is raised. Investment managers need time to work through their business plans to reposition assets and then eventually exit their positions. Similarly, fund investors are sometimes legally entitled to see a return of capital by a certain date, which may require funds to sell assets during less-than-ideal moments in the market’s fluctuation. All these things underscore how important precise timing can be to investments. Extended timelines owed to COPA could distort the flow of capital from real estate investment funds and that means curbed investment activity in NYC.

3. Lender Underwriting

COPA would impact all parties that enable real estate transactions, but one of the most affected areas would be the way loans and debt are structured. Given how fast capital markets move, lenders won’t expose themselves to unnecessary risks by promising terms and conditions that may no longer be available after 180 days. I mentioned the example of moving treasury yields earlier. But, what do extended timelines mean for issuing of term sheets? What about commitment letters, rate locks? And how do buyers of private assets get comfortable knowing their lending terms could materially change over the course of a year?

The most likely answer for lenders and buyers is that they are going to drop their prices.

Lenders will increase their spreads on U.S. treasury and SOFR yields, like they do during times of market turbulence, and this will reduce loan proceeds. Buyers will follow suit. They will lower their pricing as a means of accounting for the uncertain cost of debt.

The reasons extend beyond these, but these three represent highly applicable issues with the policy.

Not All Roads Lead to COPA

Based on the latest version of the bill 902-A, drafted on December 1, 2025 (this is not finalized), which evolved from earlier bills 902-2024 and bill 196-2022, COPA does leave some room for investors to buy and sell without restrictions. The lobbying efforts are working!

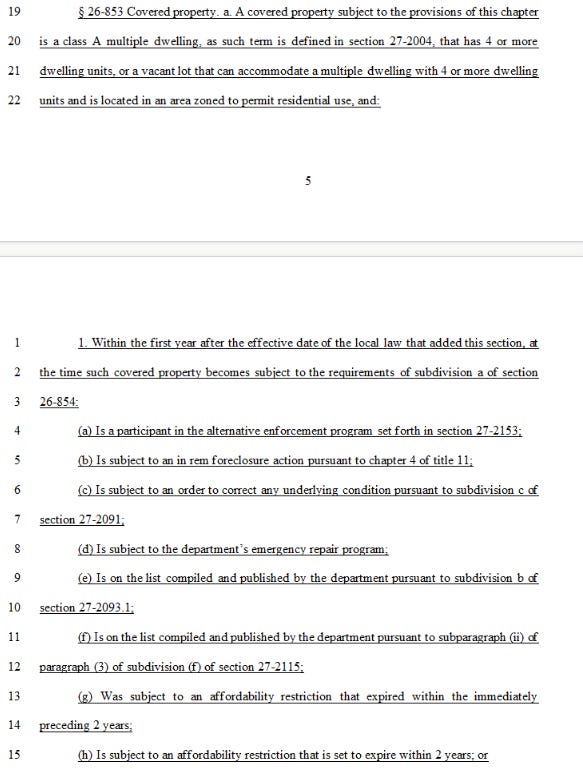

The main way to avoid COPA is to keep buildings running smoothly and avoid disrepair. Easy enough, in theory, but the devil will lie in the implementation of the policy. According to the latest bill, the following buildings are subject to COPA, known as “covered properties,”:

In short, the number of investment properties that will be subject to COPA is really very small. The majority of you reading this will not be subject to the COPA regulation when it comes time to sell, as your buildings are not:

a. In the Alternative Enforcement Program (AEP)

b. In foreclosure

c. They do not have Orders to Correct (often tied to Rent Reduction Orders or AEP status)

d. They are not subject to HPD’s emergency repair program

e. They are not subject to the Certificate of Non Harassment (CONH) program (subdivision b of section 27-2093.1 in NYC administrative code)

f. Property owners are not falsely reporting certifications of violation (see (ii) of paragraph (3) of subdivision (f) of section 27-2115 in NYC’s administrative code)

g. Fewer than two years out from the expiration of regulatory agreements

h. Currently subject to regulatory agreements

The COPA law does NOT apply to every Class A multiple dwelling with 4+ units, nor to every vacant lot that could lend itself to the development of 4+ units. It only applies to those properties that meet both the base building type (4+ units – existing or prospective on a lot) and at least one of the conditions that suggests distress and/or affordable housing. So a well-maintained, low violation 16-unit rental building in Manhattan with no liens and no expiring affordability restriction is not a “covered property” and is completely exempt from COPA. Similarly, a vacant lot in an R7A or R8 zone is not covered unless it also satisfies one of the distress/affordability triggers, which is rare for vacant land, so almost no vacant lots will be covered in practice (save maybe for those in mandatory inclusionary housing locations).

In Closing

COPA is a serious piece of legislation, and no multifamily owner or investor should treat it lightly. All investors should know about the rule and its potential impacts on the market. A forced 6+ month delay and the possibility of a mandated nonprofit buyer are real risks that can soften pricing, complicate financing, and throw tax and fund timelines off track.

That said, the current bill is a dramatically scaled-back version of what was making headlines just a few weeks ago. Sustained pushback and thoughtful amendments have narrowed the definition of “covered properties” to a small slice of truly distressed or affordability-restricted buildings. Most well-maintained, code-compliant rental properties and nearly all development sites are fully exempt. As the bill now stands, for most owners and investors, COPA will simply never apply when it comes time to sell.

Stay informed, keep your building in strong condition, and keep a close eye on the regulatory environment. For now, COPA has evolved from an existential threat to more of a headwind in a market that remains fundamentally sound.

Sinclair Realty Group is ready to evaluate and break down the latent risks of doing business in NYC multifamily real estate. The regulatory environment is constantly changing and is not friendly to outsiders. Please reach out at rs@sinclairrealtyco.com if you would like to learn more about COPA.

I am bullish on NYC Multifamily

Best Regards,

Romain Sinclair

646 326 2220

Even if your building is arguably not covered buyers Wii still shy away worried that someone will challenge

That assessment. And what about tenants make baseless charges to HPD?

Fortunately City Council has made significant changes (as of Friday 12/12) to the proposed bill. No longer a market paralyzer, but I worry it’s only the tip of the iceberg.