Insurance for rent stabilization

Why property insurance costs have increased + a new insurance product in NYC for RS building owners

Rising insurance costs together with the fleeting availability of insurance carriers willing to write new policies are eroding the profits of developers and owners of multifamily properties. Also, in NYC a new brand of insurance has emerged that an increasing share of owners may seek to purchase!

Why insurance costs have increased

Multifamily insurance pricing has gone up in the United States in the last few years. According to a research report by NMHC, which surveyed 160 apartment investment firms representing 1.6 million apartment units, owners have seen their property insurance rates go up on average by 26% since last year. There are four core reasons why.

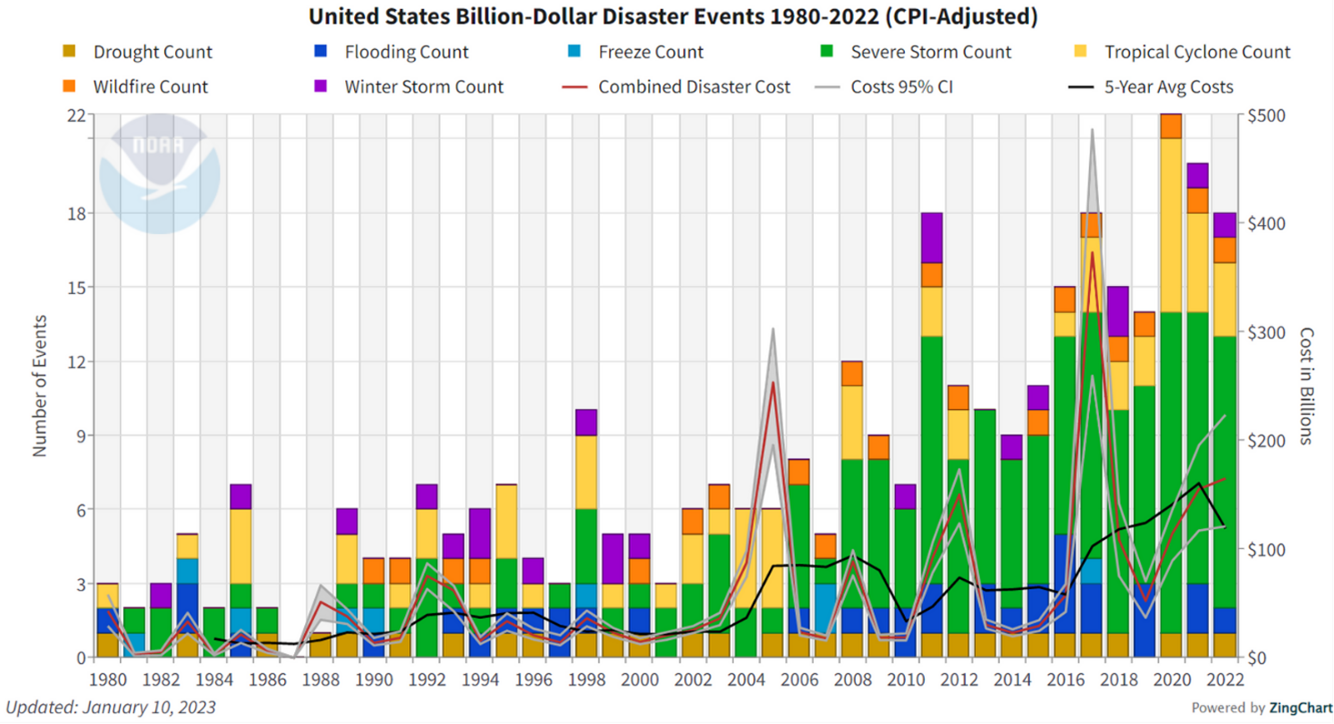

1. Climate risks: greater frequency and intensity of extreme weather patterns

Some especially notable and costly events of recent memory:

Texas freeze - February 2021

Hurricane Ida - August 2021

Hurricane Ian - September 2022

2. Inflation risk: replacement costs have increased due to elevated costs of construction

Inflation has raised the costs of construction materials, labor, and natural gas/fuel. The cost to pay your team, to order the materials, and to have the materials shipped is up. That means, if or when that natural disaster strikes, a building owner should expect to get a pay-out that is abovethe initial purchase price. This is good… except if you are an insurer.

3. Passing the buck

Insurers can offset hefty payouts to property owners by (1) reducing future coverage, (2) raising annual deductibles, or (3) raising yearly premiums. This is exactly what they have done. The same NMHC study revealed that:

Over a third of respondents’ insurance carriers lowered their coverage amounts.

61% of respondents’ insurance carriers raised their deductibles.

57% of respondents’ carriers carved out policy limits to reduce the number of cases where payouts would be allowed.

According to Matthew Rieger CEO of Coconut Grove, a large affordable developer in Florida, “when wildfires hit California, […] premiums in Florida went up.”

4. Supply shocks: insurance carriers are leaving major markets

All State and State Farm have both decided to stop underwriting new insurance policies for business and personal property in California due to the wildfire risk. It stands to reason that, if fewer carriers offer their services, and that the risk of property damage only increases, the remaining insurers will be in position to collect more fees from policy holders.

The insurance issue is prominent enough that the Senate held a committee hearing on the subject. Titled “Perspectives on the Challenges in the Property Insurance Market and the Impact on Consumers,” It is about 2 hours long and available at the previous link.

NYC Rent overcharge Insurance

On top of these national drivers behind higher insurance costs, New York owners of rent stabilized multifamily properties may consider buying rent overcharge insurance. The rent overcharge insurance would act as a shield to protect earnest purchasers of real estate from being encumbered by costly litigation that arises from tenants and others claiming rents are not what they should be. This is especially important now that regulations are way up in the market.

The passing of 2019’s Housing Stability and Tenant Protections Act (HSTPA), made owning an apartment building in NYC fraught with more risk. The 2019 act widened the “look-back” period wherein a third party could peer into a building’s building permits, DHCR rent histories, and tenant lists to determine whether the rents currently being charged were achieved according to the rules. Now, a package of bills lie at Governor Hochul’s desk that would further tighten the screws on landlords.

The current bill S2980c would mandate that owners obtain and preserve records of jobs performed on buildings and receipts and invoices for said jobs done prior to their ownership of the building. If issue is found with the way rents were raised 10 years prior to the new owner’s possession of the building, he or she would nonetheless be liable for overcharging tenants on their rents today, due to the error (purposeful or not) that put the rents on the wrong path years ago.

The insurance offering will grant protections for legal expenses and will also cover any rent overcharges and penalties determined by the DHCR. The maximum coverage limit per building is $2 million. The premium, which amounts to approximately 10% to 15% of the coverage amount, is a single upfront cost paid during the closing process. This coverage will remain effective for a period of two to five years, depending on the specific policy evaluation. Essentially, it serves as a contingency plan that will be added as an endorsement to a rep's and warranties insurance policy at the time of closing.

According to Investopedia, publicly traded companies include footnotes in their earnings reports when citing a possible liability. A probable liability is likely enough to happen such that the expected expenses or costs associated with the liability must be reported on financial statements. Possible liabilities are worth mentioning, but they are not real enough to model out their impacts on cashflows.

In case you missed it, Varney Company is pioneering the launch of this new insurance product! Reach out to their team if it sounds of interest!

Sources: The Real Deal, Multifamily Dive, NMHC survey

Loved this post, Romain! Keep it going