Insurance, Hurricanes, & Tax Abatements

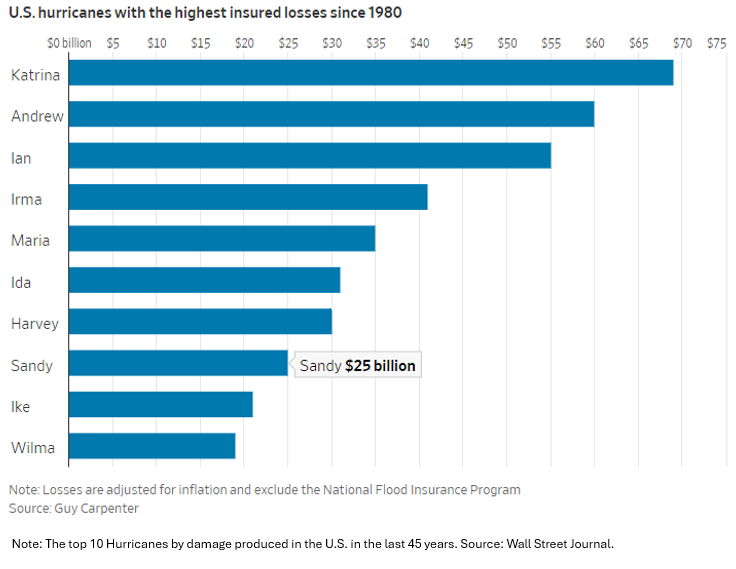

The credit rating firm Moody’s estimates that Hurricane Helene will result in damages as high as $26 billion and much of that will be from private property damage. This estimate ranks Hurricane Helene as more disastrous for the U.S. than Hurricane Sandy in 2013, in terms of damages, ranking it as the 8th most destructive U.S. Hurricane since 1980.

What's different about this hurricane– the loss of life and general chaos it has caused is similar to others– is that property insurers have grossly pulled back. Owners will have to face more considerable out-of-pocket costs than before. Some anecdotes from the article are damning:

"It's going to be much more difficult for owners of small businesses and multifamily properties as they rebuild to find insurance that isn't three or four times what they were paying before." – Alexandra Glickman, head of Global Real Estate and Hospitality at insurance company (giant) Arthur J. Gallagher.

Fewer than one in 100 households in the worst-flooded inland counties have flood coverage - Mark Friedlander, spokesman for the Insurance Information Institute, an industry group.

Around 50,000 claims are unresolved from Hurricane Ian's destructive path two years ago in Florida – with 18,000 claims that haven't seen any payouts.

The data doesn't suggest that investors, homeowners, and business owners will find immediate remedy or solace by going to insurance companies. Quite the opposite, insurance experts are saying that there will be challenges. Insurance agents say insurers offer "reduced payouts for older roofs, limits on interior water damage and exclusions for damage from wind-driven rain," and higher deductibles for wind damage. In other words, insurers will do everything in their power to avoid having to accept claims from policyholders affected by natural disasters and fork over cash.

What Does This Have To Do With NY Multifamily?

The climate events unfolding in the southeastern United States do and don't relate to NYC real estate. NY building owners are far from the eye of the storm, and they will not need to file any insurance claims on NY assets (knock on wood).

On the other hand, investors most impacted by the rent laws of 2019 and investors that would have invested capital in NY have diverted their capital towards areas with strong demographic trends and landlord-friendly policies. That means investing in the Southeastern US and the states along the Golf Coast, amongst others. Investment dollars meant for NYC property have gone to areas where the bulk of in-country migration has happened in the last two decades. These migrations have incidentally happened in areas most prone to climate disasters. Americans have embraced areas with greater propensities for forest fire, flooding, hurricane, and landslide risks. That means a contingent of NYC investors who have historically invested in NYC multifamily are at risk because they own properties within hurricane paths – historically or in the path of future storms. Even if investor properties were not hit with Helene or Hurricane Milton, insurance premiums on their properties in surrounding areas, all other things held equal, will go up heavily.

Yet, the damage caused by hurricanes could pose trouble even for property owners who haven't left New York and remain committed to it. If a storm happens in the South East, premiums in the North East go up (this was said by an insurance executive, I am struggling to find the exact source). When insurers make big payouts due to natural disasters, they will find ways to re-coup those funds. Insurance actuaries will develop detailed models to price out how to offset fringe disaster scenarios. Those models find ways to plug these insurer losses by limiting what coverage the policyholder gets or increasing his or her premium.

At insurance renewal time, investors with properties in the city find it difficult to secure policies with only modest premium increases without hefty coverage carve-outs. Anecdotes and empirical data I have reviewed suggest insurance costs have climbed aggressively for multifamily property owners – both in coastal regions and New York City. Owners have shared stories of roller-coaster-like insurance premiums with costs ballooning in Year 1, coming down significantly in Year 2, before finally landing somewhere between Year 1 and Year 2 in Year 3.

Optimizing insurance costs is a priority for owners because it is typically the second or third largest building expense after property taxes and repairs & maintenance. I see insurance policies priced anywhere from $1,200 per unit to +$4,000 per unit. The insurance market is filled with turmoil, and carrier shutdowns and insurance policies are littered with fine print and exceptions that, now more than ever, need to be read. Good insurance brokers will see the problematic insurance conditions as opportunities to provide owners tailored coaching and advisory on insurance policies. That is a good thing wrapped outside of a brutal reality. Insurance costs make up ~20% of total building expenses and events like Hurricanes Helene and Milton will only make the numbers go up.

The single largest expense for many multifamily owners is property taxes, and prospective purchasers should rejoice in knowing that, unlike insurance, there are ways to fix those expenses. The two most straightforward ways to fix property taxes are to invest in or purchase tax class-protected assets, which I have written about here, or to buy properties with tax abatements, which I have written about here and here. The strategy with both buying tactics is the same– buy properties that cap the amount of taxes owners are responsible for yearly.

The downside of tax protection was that it didn't scale because it required the purchase of smaller properties. The problem with purchasing tax abatement properties was that it meant investing in potentially declining-NOI assets (when the abatement expires and taxes jump). These downsides are essential but aren't as significant as previously thought. Carlyle and other investors have bought scattered site small buildings in Brooklyn and made a profitable business out of it.

Investors must weight the concern of "declining NOI" assets after tax abatement expiry against the alternative that was created in 2024 when Good Cause Eviction passed: buying properties with uncapped taxes that, in most cases, will have caps on gross income growth (rent growth). Further, as I have written about, tax-abated properties have pathways to eventually becoming fair markets. Investors will want that when the alternative is full taxes and restrictions on rent growth.

With the advent of Good Cause Eviction and HSTPA, New York investors know that property revenues and sustained revenue growth are not guaranteed. Considering that, having predictable or even controlled cost increases is extremely important to contribute effectively to profitability. Controlling property taxes, one of the largest and fastest-growing expenses can make for a very advantageous strategy.

I am bullish on NY Multifamily.

Call me at 646 326 2220

Best Regards,

Romain Sinclair

Source: Wall Street Journal