Mamdani and Multifamily

Rent Guidelines Board (RGB) Rent Increase Decisions Released Today

Zohran Mamdani is the presumed winner of the 2025 Democratic Mayoral Primary Election, now that former Governor of NY Andrew Cuomo has conceded victory. This is significant because candidates who win their primaries often succeed in general elections. This was the case with mayors De Blasio, Bloomberg, Dinkins, and Koch (who beat Mario Cuomo), so there’s at least 50 years of precedent for primary winners coming out on top. That means the business community, in particular real estate operators, needs to understand the opportunities and drawbacks that may arise from a Mamdani mayoralty.

Mamdani has a few different housing-related priorities, such as increasing landlord accountability to tenants, doubling down on public sector property development and management, and creating a new housing plan that hopes to create 200,000 apartments over 10 years. But, his most divisive policy is his Freeze The Rent idea.

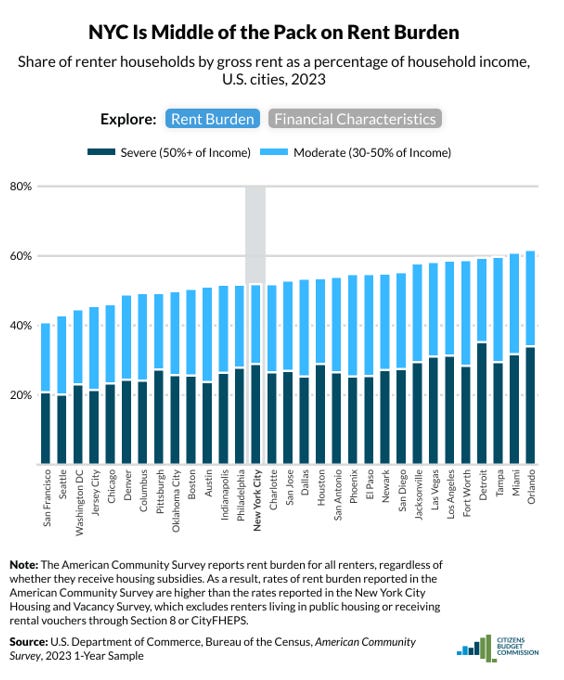

The rationale for the rent freeze is well understood. NYC is exceedingly unaffordable in general, and apartment rent in a city where 68% of residents rent represents the largest single expense to most New Yorkers. In fact, 52% of New Yorkers contribute over 30% of their gross incomes to rent. And among these, 29% of New Yorkers contribute at least 50% of their annual wages to cover rent payments. By freezing the rent, Mamdani aims to alleviate a major pressure point for renters.

Fixed Revenues and Floating Costs

But, the problem with implementing measures like freezing rents for some (because the policy would not target all apartments) NYC tenants is twofold. First, in a post-Housing Stability and Tenant Act (HSTPA) world, thousands of buildings in New York have operating expenses that meet or exceed their revenues. Over time, if building rents do not cover expenses, buildings will fail. Like any business, there has to be an expectation of profitability. Otherwise, the operation of privately-owned buildings would be an exercise in goodwill and philanthropy. Current laws and frameworks for rent increases, which include RGB increases of 2.75% and 3.0% the last couple of years, are not satisfactory for covering expenses. Adding four consecutive rent freezes into the mix further exacerbates the issue. This has been covered in depth in a few important articles of research here, so I won’t belabor the point:

Community Preservation Corporation (CPC) – NYC Rent‑Regulated Portfolio Data Brief (2020–2024).

In their research, CPC finds that “CPC's per unit expenses have grown 22%, while the RGB permitted a roughly 11% cumulative increase to stabilized rents over that same time,” from 2020-2023.

Senior Policy Fellow Mark Willis, NYU Furman Center at his RGB Testimony - HSTPA and the Challenge of Preserving NYC’s Unsubsidized and Subsidized Affordable Housing Stock.

In his testimony to the Rent Guidelines Board (RGB), Willis points out that many rent‑stabilized buildings, especially in the Bronx, are operating at a loss—some losing on average $120 per unit per month, particularly post‑HSTPA‐2019. He goes on to say, “The real estate industry has been complaining for a long time, so how do we know that post-HSTPA is any different? I think what you can take away from [the numbers] is that this is real. There will continue to be rent shortfalls that grow over time under the current system, and that is not going to turn out well."

Bisnow Overview of Privately Owned Multifamily Portfolios – ‘The Crisis Has Already Started': Inside The Finances Of 4,300 Rent-Stabilized NYC Apartments.

Bisnow’s analysis of nearly 4,300 apartment units reveals declining cash flows across the board.

Rent Guidelines Board (RGB) – 2024 Income & Expense Study (I&E).

9.8% of buildings surveyed had operating costs exceeding revenue (i.e. “distressed”)—up from pre‑pandemic lows. And operating costs per unit were $999.

NYU Furman Center – “The Economic Challenge for the Rent Guidelines Board:

Preserving Affordable Rent Stabilized Housing for the Long Run”

Underscores that constrained rent growth combined with unconstrained, rising operating costs creates long‑term preservation risks for affordable housing.

Concentrating Demand on a Small Supply Base

The second problem with freezing rents for some tenants is that it makes rents for those not receiving freezes grow more quickly.

There are approximately 1,000,000 rent-stabilized housing units, and then about 250,000 units of public housing, rent-controlled units, or other specialty programs not subject to fair market rents. Most of the rental housing supply in NYC is regulated.

When a million apartments have their rents frozen, tenants in those apartments will typically avoid moving. According to the New York City Housing and Vacancy Survey of 2023, the vacancy rate for rent-stabilized housing in 2023 was 0.98% and the vacancy rate for fair market apartments was 1.84%. In other words, rent-stabilized tenants already commit to their apartments more than their generally more affluent counterparts in free-market apartments. When we examine specific rent levels, the trend lines are more pronounced and easier to see. In 2021, apartments that rented for over $2,400 per month experienced four times the rate of turnover compared to those rented for under $1,100 per month (44% vs. 11%).

So where’s the problem? And what does the vacancy rate and turnover have to do with the affordability crisis?

Well, if half of the NYC housing stock sees its turnover shrink to near 0% levels, half of the housing supply in NYC is closed off. This means every fall, when large waves of demand for apartments come crashing down on NYC, there will only be half of the available housing supply to meet that demand. That makes renting more competitive for renters. It lowers the standard apartment quality, as renters don’t have the luxury of choice. Most importantly, it makes rent more expensive.

Good Cause Eviction attempts to solve this problem by capping rent increases on fair-market housing units. But there comes a point where it’s tough to legislate away the problem of a constrained housing supply. Landlords will obtain new Certificates of Occupancy (COs) to bypass the Good Cause requirement. Or, they will pivot to new construction projects exclusively. To put it succinctly: what happens when rents are capped in one segment of the market is that they grow like hell in other segments. The average rent growth of 94.2% in Greenpoint-Williamsburg over the last two decades effectively demonstrates this. Emphasis on the word average here.

In summary, freezing rents without a corresponding tax abatement or price cap on expenses for properties in NYC wouldn’t be beneficial for the sustainability of the housing stock. Doing so would lead to declining apartment housing conditions for tenants across the city due to untenable property maintenance costs. This might feel great during Mamdani’s term, but any succeeding mayor would have to deal with a rent-stabilized housing stock that is worth than it is today. On the other hand, creating rent freezes will choke off half the housing supply and induce even greater upward pressure on free market rents. Even if annual rent spikes can be kept in check with Good Cause Eviction, it would mean consistent rent increases of 8%, or invite private investors to find methods to circumvent these caps. For these reasons, I think the rent freeze is a shortcut to finding a real solution to the housing issue. Next week, I will consider whether a rent freeze would even be possible for Mamdani to undertake under the current conditions in NYC.

**Rent Guidelines Board Decisions Announced Tonight at 11:59PM.**

I am bullish on NYC multifamily.

Best Regards,

Romain Sinclair

646 326 2220

Sources:

Bisnow. (2024, February 8). ‘The crisis has already started’: Inside the finances of 4,300 rent-stabilized NYC apartments. https://www.bisnow.com/new-york/news/affordable-housing/the-crisis-has-already-started-inside-the-finances-of-4300-rent-stabilized-nyc-apartments-129459

Citizens Budget Commission. (n.d.). A more competitive NYC: A plan for the city to win back jobs and residents. https://cbcny.org/competitive-nyc

Community Preservation Corporation. (2024, May). CPC NYC rent-regulated portfolio: 2020–2024 data brief. https://communityp.com/wp-content/uploads/2025/05/CPC-NYC-Portfolio-Data-Brief-2020-2024-v2.pdf

Furman Center. (2024). Economic challenge for the Rent Guidelines Board. https://furmancenter.org/files/publications/Economic_Challenge_for_the_Rent_Guidelines_Board.pdf

Mark Willis. (2024, June). Testimony before the NYC Rent Guidelines Board. NYU Furman Center. https://furmancenter.org/files/Preservation_Challenges_RGB_testimony_Version_III_April_10_final.pdf

New York City Department of Housing Preservation and Development. (2023). Selected initial findings of the 2023 NYC Housing and Vacancy Survey. https://www.nyc.gov/assets/hpd/downloads/pdfs/about/2023-nychvs-selected-initial-findings.pdf

New York City Rent Guidelines Board. (2024, March). 2024 income and expense study. https://rentguidelinesboard.cityofnewyork.us/wp-content/uploads/2024/03/2024-IE-Study.pdf

Sinclair, R. (2024, December 5). What would a rent-stabilized grocery store look like? Sinclair Substack. https://rsinclair.substack.com/p/what-would-a-rent-stabilized-grocery

Zohran for NYC. (2025). Zohran Mamdani for Mayor. https://www.zohranfornyc.com/