National Multifamily Trends

Gleaning insights from 2024 to understand the current climate

To best understand NYC-specific trends, it’s essential to consider and be aware of the national multifamily happenings as well. Freddie Mac, Fannie Mae, Newmark, and New York Life published their views on the multifamily market in 2024 with some speculation of what’s to come in 2025. I leverage the research these groups have done to provide the insights below to those invested in or curious about the NYC market.

Multifamily is doing well at the national level. The right demographic and economic trends are in place to support sustained growth. Some examples are below:

· Investors deployed more capital into multifamily than any other type of commercial real estate in 2024. According to Newmark, 34.7% of all property purchases were Multifamily buildings last year. This is significant because it represents the ninth consecutive year above the 23-year average of 27.8%.

· The premium to own a home instead of renting remains stubbornly high. According to BLS, NAR, and Freddie Mac, that premium sits at ~90%. Newmark estimates the median monthly home payment was $1,120 higher in 2024 than what a rent payment would be for an equivalent housing unit.

· The share of young Americans (25-34) living with parents has nearly doubled since 2005, from ~11% to 16% last year. In the same vein, the segment of renters in general (no age category) that are moving out of apartments to purchase homes stands at 8.6%, the lowest level since 200,7 when it approached 20%, according to Newmark.

· New supply of multifamily is poised to decline. In the post-covid-era after 2020, multifamily permits, starts, and deliveries markedly increased. The 591,000 housing units that developers delivered in 2024 were more than any prior year on record since the data was collected starting in 1980, according to Freddie Mac.

The data tells us that investors want to purchase multifamily, and it offers us insight into why they might want to. It pays for renters to keep their status as renters rather than take leaps into homeownership. Moreover, supply/demand ratios for multifamily housing are finally beginning to re-calibrate. Whereas Sunbelt developers delivered hundreds of thousands of apartment units in the last few years (like DFW, TX), these markets have largely absorbed newly built units and are on the path to higher occupancy and rent growth.

The Headwinds

· According to Freddie Mac, the spread between average cap rates and 10-year treasury yields hovered around 120 basis points as of November 2024. That’s an average 10-year treasury yield of 4.36% and an estimated cap rate of ~5.6%. The difference between cap rates and treasury yields represented a wider spread than the 100 basis points seen during late 2023 and indicated a narrower spread than the 300 basis point difference during the early aughts.

· Because of how close cap rates are to interest rates, Newmark estimates that for deals > $5 million, investors were just barely able to secure positive leverage on debt. But, when taking a closer look and considering debt constants against cap rates, most deals in 2024 would have been purchased with negative leverage.

· Related to the above, much of the multifamily pricing gains made during the onset of Covid-19, have since been erased. Values have come down across the board from Phoenix to Atlanta to NYC. In areas like Minneapolis and San Francisco, pricing has decreased more than 10% Y-O-Y. Even the data used by Freddie Mac and Real Capital Analytics CPPI recognize the value declines in NYC’s housing stock.

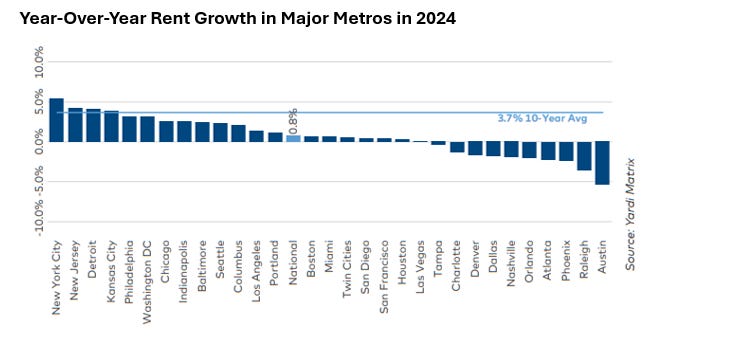

· Oversupply has hurt some markets like Austin, Atlanta, Raleigh/Durham, and Phoenix, and these markets will be behind others in seeing rent growth.

When negative leverage is afoot (debt constant/cap rate >1.0), everything gets more challenging. When the cost of debt service is greater than the cap rate, every additional dollar of debt taken on dilutes the return investors receive. Since most transactions are financed by debt, this is a problem and can really logjam the market for transactions.

Outside of the oversupply of housing issues in some markets like Austin, Atlanta, Raleigh/Durham, Phoenix, and others, NYC investors face much the same challenges as investors in the DFW market. In both metros, investors are trying to purchase properties with compelling cap rates that the GSEs will finance with tight spreads over the 5- or 10-year treasury yield curve. On the other hand, investment groups also benefit from the high cost of debt which precludes average renters from buying homes and shrinking the renter pool. The remarkable difference about NYC investing is that occupancy levels are generally higher than in other markets since demand for housing consistently exceeds supply-side deliveries – there is no ebb and flow.

2025 should be an interesting year for NYC Multifamily. Bob Knakal is known for his rule of thumb that in Manhattan 2.5% of properties trade hands each year. But in 2025, 2026, and 2027, he believes that closer to 5%/6% of the building stock will sell, effectively doubling the typical number of annual transactions. Will that come due to financial distress and loan repricings/maturities forcing owners’ hands? Will it be due to the market picking up due to the onset of some new tax relief from President Trump? Will it come at all? And how will that look in the outer boroughs? To be determined.

I am bullish on Multifamily, especially Multifamily in NYC.

Best Regards,

Romain Sinclair

646 326 2220