New York Community Bancorp (NYCB) a Few Months Later

A Mirror Into the New York Rent Stabilized Story From the Lender perspective

Editors note: When the dust settled from NYCB’s stock collapse in late January, I wrote an Op Ed (2/11) and then another one a month later (3/8) detailing my thoughts on the situation and how the distress was a product of NY multifamily regulatory issues - since, after all, NYCB was the largest lender (by loan count and avg loan size) to rent stabilized building owners by a mile. These analyses contained more forward looking statements than I usually write and I was not 100% if I had the required data available to make the predictions I made so I didn’t publish anything. Today… I’m still no banking expert, so it’s likely I’m missing some things but I also believe I get a lot right. Below is what I wrote on March 8th, 2024 and much of it I think rings true.

New York Community Bancorp, Inc. (NYCB)’s share price dropped by 25% in the last few days because of news of a $2.4bn asset write-off, effectively wiping out ~$870m of shareholder value. This comes after investors tanked the share price by 60% in the span of a few days in early February when they heard NYCB was cutting dividends by 70% and increasing capital reserves by 60% from three months earlier. Is the stock going to bounce back, or is this the end for NYCB?

The credit issue explained

NYCB’s problems today are not because of its office loan exposure. Office loan risks are understood. Older, unremarkable office properties are worth less because they will produce fewer dollars in the future than today due to work from home policies. Only 4% of NYCB’s loan portfolio is exposed to this office risk. That means NYCB is unique in this regard and the bank’s issues are not an industry trend.

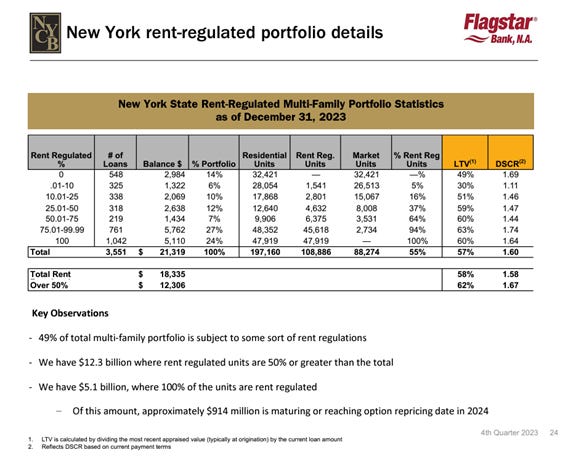

On the other hand, 44% of NYCB’s assets are loans made to multifamily properties, 80% of which are in NYC, and 49% of which are subject to some degree of rent stabilization. Multifamily loan pools are facing distress because of rent regulations passed in 2019 that reduced long term rent growth and the hikes in interest rates that instantly raised the costs of managing leveraged properties.

Example:

Let's say NYCB extends a loan of $600,000 on 123 Main Street in Manhattan purchased for $1,000,000 in 2018. That property may be worth only $700,000 today because of the more austere rent caps applied in 2019’s updated rent regulations. The leverage point of the loan goes from 60% to 85% ($600k loan/$700k property value).

This is a risky place to be, but the lender will continue to collect its monthly payments and the borrower might be able to pull off a refinance with the right lender who values the property a bit more highly. But what if interest rates also increase and the yearly debt payments go up on new loans? The pool of lenders willing to extend new loans to the borrower all but disappear. The loan is not able to be “taken out,” or refinanced for its principal balance because the asset’s income won’t exceed the debt payment by enough of a margin to get lenders comfortable. The borrower or the bank must sell the property at a discount to re-coup some cash.

Maybe the property can sell for $600k net of transaction costs. Maybe it can only sell for $500k, or ~85% of fair market price. If NYCB’s loans are paid back up to 85% of their original balances in 3 out 5 cases and NYCB has about 3,000 (3551 RS – 548 FM) loans subject to rent stabilization, that means:

3,000 loans x $6.1m avg. RS loan size x 60% loss probability x 15% loan value lost

= $1.65bn in asset values destroyed

= 2% of assets destroyed

That’s a pretty small percentage! Though my math is clearly back of the envelope using estimates about the market, most loans on rent regulated multifamily will be affected since the rent laws lowered values on all properties in NYC. Yet, the size of the loss per loan should be below 25% since NYC housing stays at 100% occupancy and rent regulated multifamily assets still hold more than 60% of their value.

NYCB anticipates $2.2bn of its rent stabilized loans to mature this year out of a possible $18.3bn, which means that approximately 11% ($2.2bn/$18.3bn) of $1.65bn of loan losses should begin this year, or approximately $194m. In its Q4 2023 earnings report (snippet shown below), NYCB accounts for a total of $992m in loan losses, a $373m (60%) increase over Q3, with no change in loan amounts. Rent-regulated multifamily makes up 1/5 of the bank’s loan book. If we apply a similar risk level (unlikely) to the remaining 80% of loans, we arrive at $970m of loan losses this year. Even at that number, NYCB is 100% covered based on its own risk provisions!

So, NYCB may have things fully under control? The dividend shrank because that capital was being re-allocated towards loan losses. Investors didn’t like the loss of cash-flow and sold their shares. That seems very plausible.

What about Good Cause Eviction?

NYCB’s problem with its rent regulated loans is contained to just 34% of its real estate portfolio, or 21% of its overall loan book, but what if it wasn’t?

“Good cause” eviction is a policy that emerged in 2020 that would cap rent increases and prevent tenant evictions for nearly all multifamily properties in New York state. Only 900,000 apartments are rent regulated in NYC today. The bill would extend the cover of rent regulations to all 2.1 million rental apartments in NYC. If NY congressmen passed the bill, it would hurt NYCB’s loan portfolio. Instead of impacting “only” 3,000 loans worth $18.3bn, the new rent regulation would clamp down on the full NYCB multifamily loan book worth $37bn.

NYCB’s Q4 Earnings Report presented a comprehensive overview of their rent regulated loans, but they failed to entertain any discussion of good cause eviction, or of a deepening of rent regulations. Investors and analysts covering the company do not seem to be digging deep enough into NYC’s overlapping layers of rent regulations and policies, both in consideration and in effect, to adequately price in the risk of good cause eviction. More shocking still, Signature bank’s loan metrics still used Loan to Value (LTV) figures based on property valuations from when loans were originally underwritten. That’s willful ignorance of the truth.

The bank will suffer credit losses from its rent regulated portfolio and that will create a drag on profitability and require additional cash reserves. If good cause passes, the magnitude of losses will likely double, because the loan amounts go from $18.3bn of impaired loans to $37bn. Yet, NYCB’s leaders had the vision to know rent regulations would hurt them and that spurred them to diversify their business through acquisitions. Buying Flagstar diversified NYCB’s loan portfolio out of NYC and the Signature bank acquisition provided diversification away from the real estate vertical. NYCB is much more than *just* NYC’s largest multifamily lender now, its brand platform is broader.

Still, investors should expect to see the share price continue to drop. There will not be a bank run on NYCB any time soon because nearly all of its deposits are FDIC insured (even the uninsured). That said, the lender’s profitability will suffer in the short term and its capital allocation will shift away from dividends towards growing its liquidity. If good cause passes and applies rent controls to more assets that the bank lent money to, which few, if any analysts, seem to be entertaining, the dividend will be cut down to $0.00 and this will trigger another sell-off of bank shares. Even considering this, the bank’s underlying business is stable, and deposits have no reason to run for the exits.

Expect some multifamily loans sale. Big time. Private-public partnerships will step up to buy the loans with the blessing of NYC’s government, just like how CPC & Related bought Signature, and how CPC & FDIC are offering funding for building owners to perform repairs. I wouldn’t be surprised if the bank made a name change either. Discounted note sales are going to be an opportunity for those who believe in NYC multifamily and are funded enough to purchase big chunks of notes.

Reflection today on May 24th, 2024

Things I was right on:

Good Cause Eviction passed - (technically not passed into law yet, but all parties agree on its passing).

NYCB’s share price declining (pretty small decline, but still)

Name change (NYCB is a lender saddles with RS debt. Flagstar is a diversified lender with a beautiful logo)

NYCB selling off its loans for liquidity (JPM is buying $5bn of CRE loans)

Where I was wrong:

No government support/bailout

What does this mean? One less capable lender to rely on as a multi family investor means higher interest rates for loans, and fewer chances of making deals pencil.

Please connect me to lenders selling notes.

I am bullish on NYC multifamily. Call me at 212 658 1471.

Sources:, NYC Q4 Presentation, NYCB Feb 15th presentation, NYB Q4 2023 Earnings report, Bloomberg News