NY Multifamily Owners: Cash it in or Cash The _ _ _ _ _ Out

Cash it in or Cash The MONEY Out... with CMBS

Cash it in or Cash The Money Out.. with CMBS

The wave of loan maturities coming to the New York multifamily market will embody all the struggles and challenges owners have put off for the last several years—the Covid arrears overhang, the crushing defeat of HSTPA, and now the skyrocketing interest rates. Investors must realize capital gains for those gains to be real, and the same goes for losses. That all changes when your lender asks you for a cash-in refinance or when you sell your building at a 10% capitalization rate. There is no one-size-fits-all solution, but today, I will do my best to highlight why investors should consider CMBS loans as a capital solution.

CMBS or Commercial Mortgage-Backed Securities are loans secured by commercial real estate that lenders create and then sell to bond investors. The investors who buy loans trade their cash in exchange for future cash flows, and lenders sell these loans to create more liquidity for themselves and allow them to go out and generate more loans. These have grown in popularity – both inside and outside of New York. Let me attempt to explain why.

First, some more basics on CMBS loans:

Lenders structure loans as interest-only. Borrowers pay no principal for the loan term, with a balloon payment due at the term's conclusion.

Prepayment penalties for early loan repayment are more nuanced than step-down penalties (e.g., 5-4-3-2-1 schedules) and can be more punitive or rewarding.

After creating the loans for borrowers, lenders will package the mortgages into loan pools and then sell tranches of the loan pool to bond investors.

Important Insights:

When interest rates go up, the difference between amortizing loan payments and interest-only payments grows smaller and smaller. That means lenders that offer CMBS non-amortizing loans today make comparatively more money per loan than on the same loan in a low-interest rate environment. CMBS Lenders today love this. Since the debt service is so close to an amortizing loan, all it takes for the CMBS lender to obtain full amortizing loan yield is to bake in a few small or big fees for the total profits on the loan to meet or exceed that of comparable amortizing debt.

CMBS lenders can also underwrite loans more aggressively. The annual debt service is lower because CMBS debt is usually interest only. This lower debt service lifts the DCR constraint that sometimes caps the size of loans. In practice, that means that for the same $1.00 of net operating income a building produces, $0.83 will go toward CMBS debt payments. Amortizing loans of the same size for the building will eat $0.93 for every $1.00 of NOI produced. The 'High Rates’ column in the table below highlights this point. The 'Low Rates’ column reminds us just how different things were in 2021-2022. In the example below, the CMBS loan offers 12% more in loan proceeds than an amortizing DCR constrained loan.

CMBS lenders would benefit from rebranding their defeasance prepayment penalties as hedges against market fluctuations because that's the truth in many ways. Defeasance prepayment penalties require mortgage holders to purchase baskets of securities to replace the monthly payments to the bondholders that have 'bought the loans' from the original lenders. Bondholders are investors who want to invest their capital in assets with the highest risk-adjusted returns. When the returns your loan offers them are above market, they don't want you to pay off the loan early. If you do, they will penalize you and ask you to buy enough government treasury bonds to replace the yield they would have gotten for the remainder of the loan term. No one likes penalties, but penalties happen when the market picks up, and rates drop, which is good. When your loan costs you a higher interest rate than what is on the market, it may benefit you to refinance your debt.

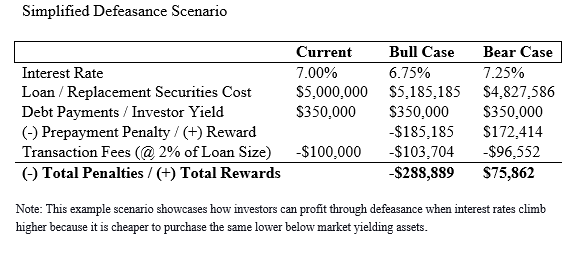

CMBS defeasance can also be a valuable option when mortgage interest rates increase. Better investment opportunities will become available when fixed-income returns are better than those on the borrower's loan (tranche of the loan pool, technically). Bondholders will lose interest in the borrower's comparatively lower loan payments. They will want borrowers to prepay loans. Defeasance is structured to encourage early prepayment when rates rise, allowing borrowers to buy discounted treasury bills such that their yield matches the loan payments bondholders received. The only difference is that when rates go up, treasury bills are cheaper. A $1000 T-bill with a 7% return may be available today for only $972. A $30m loan could present $840,000 in savings before transaction fees. Sometimes called a negative defeasance prepayment penalty, defeasance can reward borrowers and building owners when interest rates increase - acting as a very effective hedge no matter how the market moves. Look at the table below for an example of defeasance when rates move down in a Bull Case and when they move up in a Bear Case.

CMBS loans are not for everyone, but perhaps in the right situations, CMBS lenders can act as a portal to higher loan proceeds. For borrowers who face Cash-ins because of NY rent regulations, this could offer a pathway that prevents cash-ins or forced sales. Call me to discuss how to avoid a sale and go this route instead. If you disagree with any of the above, please leave a comment.

I am bullish on NY Multifamily.

Call me at 212 658 1471.