Protecting your deposits through periods of uncertainty

The consequences of Silicon Valley Bank (SVB) and Signature Bank going under will be broad and discussed for some time as regulators, economists and bankers ponder how to manage risks better. In case you missed it, both lenders suffered from bank runs, where depositors rushed to pull funds out and this forced the lenders to short sell assets and try and meet those obligations.

But what’s the implication for multifamily investors and borrowers in NYC?

>>Moving Away from one bank relationships<<

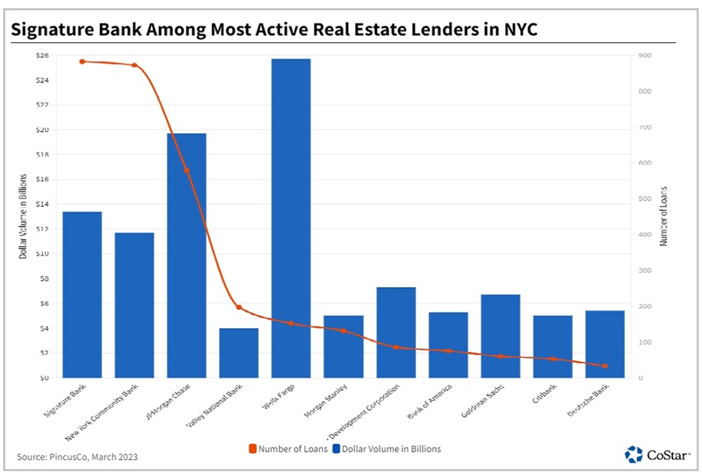

According Law360 and other sources, relationship banking will suffer as a result of this shift. Community Banks like Signature Bank funded billions of multifamily loans annually in NYC – Signature bank’s loan portfolio was $35.5bn prior to its fall (see page 18), +$20bn of which was composed of multifamily loans. Less than 10% of customer deposits were below $250,000 at Signature Bank, the limit for insurable deposits. Were it not for the federal government stepping in and saving these deposits, billions could have been lost by multifamily investors in New York.

Since the start of 2020, Signature Bank issued about $13.3 billion across 882 loans

I see three key options that investors can take to proceed with prudence and protect their funds:

1. Open accounts with different banks.

This is what Milwaukee Bucks NBA player Giannis Antetokounmpo did. The star racked up an impressive ~$150MM through the NBA at the age of 28, and had about 50 different bank accounts so as to insure all his funding. This is not a good idea usually, but it could become more viable now as a fail safe approach to preserving funds.

2. Flight to quality

Or you could do what Marc Lasry, part-owner of the Milwaukee Bucks, told Giannis and bank with the big, national banks. JP Morgan Chase, Bank of America and others. The thinking is that large, national banks might be too big too fail, and that they also are subject to more stringent rules that community banks are not subject to, which offer more protection to depositors. This type of thinking was on full display over the last few days as Bank of America (BOA) saw a whopping $15Bn increase in deposits in the last 4-5 days alone. Signture Bank had $88.6Bn in deposits when it fell. That means BOA snatched the equivalent of 17% of Signature Bank deposits in just days.

3. CDARS

My favorite option is to leverage Certificate of Deposit Account Registry Services (CDARS). CDARS allows one to deposit several million dollars into Certificate of Deposit Accounts and have them still be FDIC insured (read more about it here) via a network of lenders all agreeing to insure the funds. Neat trick, and available at 3000 banks, local and national.

Sources: Law360, Bloomberg, The Real Deal, Globe Street