SEC Looks at NYC Lender's Rent Stabilized Loans

Market Update: Please join Dan Marks CEO of Terra CRG for a 15-minute zoom webinar tomorrow at 12PM ET where he will share insights on Brooklyn’s Investment Sales activity in Q4 of 2024, reflect on the past year, and provide forecasts for 2025. Link here to register.

Concern about the ‘wall of maturities,’ or the wave of expiring commercial real estate mortgages in the United States, and what that could mean for NYC banks holding rent stabilized loans has reached a critical juncture, and now the Securities and Exchange Commission (SEC) is getting involved. The SEC identified some publicly traded multifamily lenders with concentrations in NYC rent stabilized properties and drilled down on their quarterly financial reports with some questions. What does the SEC’s line of questioning portend for multifamily building owners? What does it mean for bank shareholders? And what of the banks themselves – how might that scrutiny impact them?

From the Horse’s Mouth

The SEC questions bore down with an emphasis on Flagstar Bank, or NYCB, as it was known before its rebrand in October 2024, and it's interesting to consider NYCB's comments about its loan portfolio and its view on the economic outlook. Before I dive into that, consider reading my previous posts about NYC banks with rent stabilized loan exposure here, here, here, and here that introduce some of the challenges banks have been through because of rising interest rates and the drop in value of NYC rent stabilized buildings.

NYCB is open about some of the risks surrounding it:

Liquidity: There are fewer new deposits because fewer new loans, which require deposits, are being originated, and fewer loan payoffs are happening. Conversely, there is the risk of banking deposit outflows. About $16.6bn of Flagstar's deposits, or 20% of the lender’s $83bn in deposits, are uninsured by the FDIC. Less money in deposits reinforces the downward cycle of fewer loans made and fewer deposits received, which weakens the bank's long-term viability. (page 88, of Q2 10-Q).

Business: The bank concedes that the New York Housing Stability and Tenant Protection Act (HSTPA) of 2019, considered "the most extensive reform of New York State's rent laws in several decades" (NYCB's Q2 10-Q), has had an impact. The official language in the Q3 10-Q stops short of using condemning language, but it does specifically highlight the HSTPA. Other concerns connected to this one are the general economic conditions in NYC since so much of the NYCB loan portfolio collateral comes from the built environment in NYC. (page 89, of Q2 10-Q).

Legal and Regulatory: Scrutiny from U.S. bank regulators and new compliance that the lender must abide by are also concerns. Since its purchase of the Signature loan portfolio, NYCB has assets under management of over $100Bn, which requires it to follow another set of rules smaller banks need not worry about. There are also concerns over the existing management team's savvy around risk management procedures.

However, out of all these concerns, the most important one that will keep borrowers up at night is how the bank will deal with upcoming loan maturities. If the lender sells groups of loans at discounts, that could enable borrowers to perform necessary loan modifications. When the loan modifications happen (there is no if here), will also be critical to how this process works and how favorable/punitive a loan modification will be to the borrower/lender.

When Do The Problems Happen?

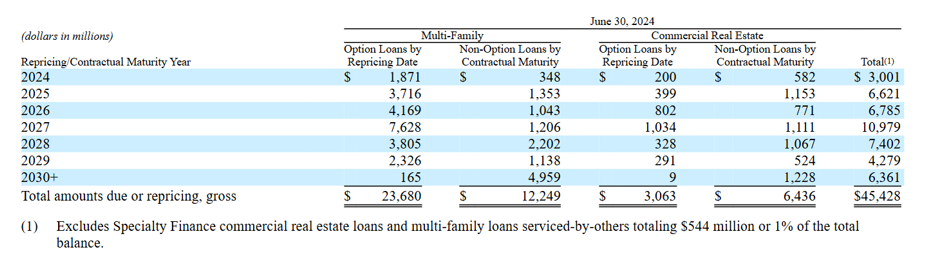

In NYCB’s second quarter 2024 financial report (Q2 10-Q filing), the lender spells out its loan repricing/maturity schedule for the next 5+ years.

Some key insights from the chart above:

The total loans due or coming up for repricing will more than double YOY in 2025.

The number of multifamily loans coming to maturity in 2025 will be fivefold that of 2024, representing a ~400% increase.

In 2026, multifamily & commercial loans coming due/for repricing will stay consistent with 2025.

Multifamily loans to be repriced in 2027 will quadruple those that were repriced in 2024.

According to the SEC, “63% of the total [NYCB multifamily loans] will mature or reprice in the next five years,” and the table above corroborates the SEC, showcasing how close to $30bn of loans will come due for repricing or maturity in 2027.

If Fed Chair Powell had been right four years ago, inflation would only have been temporary, and interest rates would have remained low, meaning a rate reset wouldn't have been a bad thing, but that is not the world we live in today. A rate reset for a permanent loan originated prior to 2022 can mean a doubling of interest rates. What’s more, the capital market expectations don’t suggest there is any light at the end of the tunnel for a rate lowering anytime soon. Chatham Financial offers the chart below to say that the yields on mid to long-term treasuries are going up over the next 10 years.

This chart, which makes the case that treasury yields today are at their lowest for the next ten years, is not good news for building owners because the higher the treasury yield goes, the more expensive debt becomes and the lower the value of real assets. This is especially hard for assets that cannot offset inflation by increasing rents. In short, rate resets or upcoming maturities represent negative, painful events for building owners and lenders who are betting on payoffs from those owners.

Now that we have a sense of when to expect problems due to expiring NYCB loans, it's important to understand how many loans are/will be problematic. Interest-only debt is the first place to look because of the increase in monthly debt payments that happens when interest-only loans begin to amortize. And, according to NYCB:

“The multifamily loan portfolio had $15.4 billion in loans outstanding that were in their interest-only period as of June 30, 2024 (…) Historically, we originated certain loans with an initial interest-only period, which was typically 24 months or less. However, the policy allowed for the interest-only period to exceed 24 months. From 2020 to 2022, most multifamily originations contained an initial interest-only period. The loans originated in that timeframe with initial interest-only periods included lower leveraged loans that had interest-only periods over 24 months.” – NYCB response to SEC inquiry.

Out of ~$45bn in CRE and multifamily loans, one-third of the portfolio, or ~$15bn worth of loans, were in their interest-only (IO) periods 6 months ago. The IO periods for many of these loans were two years or less. But for some loans, there were presumably three years, five years, or even full-term interest-only payments. According to the SEC and NYCB, 38% of the $18.5bn in rent stabilized loans are interest-only. That is a big number!

That much interest-only debt on RS property is a problem. The lender may have originated these loans before 2019’s rent regulation laws, but that would mean the IO period was full-term on those loans because it’s now been over five years since June 2019, which is imprudent. Or, as NYCB seems to confess, the lender originated these IO loans more recently on property that is rent stabilized, and the IO period is only a handful of years soon to burn off. Both scenarios reveal a risky approach, but the latter may be better because IO debt could be used on 50/50, FM/RS buildings to enable repositioning. Short of paying off loans in cash, investors must eventually replace IO loans with amortizing loan payments in nearly all cases. Those loan payments will swell once they begin amortizing. And, according to NYCB’s Q2 10-Q report, there will be a lot of transitions from IO to amortizing loan payments coming down the pike – to the tune of $4.2bn (60% of $7bn).

“The weighted average interest-only period remaining was 22 months as of June 30, 2024, with approximately 60 percent of these loans entering their amortization period by the end of 2025.” -Q2 10Q report

Receiving principal payments on loans is an excellent thing for NYCB. But, it also presents a big uncertainty – will borrowers be able to fulfill their debt service obligations when the payments materially increase? Imagine a loan was originated in 2022 and begins amortizing in 2025, only to then be up for repricing in 2027. Now imagine that scenario on an asset that has a maximum of 1% NOI growth during the same period. That adds a lot of pressure on borrowers.

Some borrowers will have taken on low-leverage loans and been conservative, while others may not. Interestingly, NYCB partially deals with the issue of future credit risk by kicking the can down the road.

“Upon receipt of updated borrower financial information, we perform an analysis to determine whether the cash flow from the underlying collateral is sufficient to meet the contractual loan payments, commonly referred to as the debt service coverage ratio. We consider the ability to cover debt service based upon the current contractual rate, or where a borrower’s initial fixed rate period expires within 18 months, the lowest contractual rate reset option available under the loan terms using the current level for referenced indices. Loans for which the collateral does not have a debt service coverage ratio of 1.0 or higher under this analysis are rated substandard” - NYCB response to SEC questions

In other words, NYCB doesn't consider loan maturities more than 18 months out when considering whether borrowers can adequately service their debts. That means risk officers at NYCB would not include a loan expiring in Q3 of 2026 in their analysis were it done today. On the one hand, it’s understandable to take this approach. Projecting the future capital markets environment beyond 18 months is a tall task. To do so while also creating assumptions for what rent and operating expense growth will be– is quite tricky. But then again, over half of the multifamily loans are collateralized by rent regulated buildings with flat net operating incomes, making projections significantly easier. The core problem with the RS loans isn't that interest rates increased but it's that the HSTPA materially devalued the collateral assets. Projecting pro forma debt service coverage with some slight room for error shouldn't be too laborious, if building rent and expense growth is correctly forecast. Lenders have everything they need to predict whether borrower collateral assets will have trouble supporting debt for the next five years.

Advice for NYCB borrowers:

Borrowers facing loan maturities or repricing deadlines, whether with NYCB or other lenders, are struggling. Many community banks are 'pencils down' on rent stabilized buildings. Suppose lenders are open to underwriting these assets. In that case, they are closed off to all but the very lowest LTV values because of elevated DCR requirements, which doesn't help borrowers seeking cash-neutral refinancings. CMBS loans can work for investors who need higher LTVs and don't mind big closing costs and hefty prepayment penalties. Ultimately, the best path forward for borrowers is to trigger reappraisals with lenders to obtain lower building valuations. If that occurs, properties can be approved for lower-priced sales, and/or part of the loan can be counted as a 'charge off,' with a certain amount of unrecoverable money. The key part of this approach is to trigger reappraisals. To obtain reappraisals, borrowers must submit the most up-to-date operating statements. To meet the threshold for distress… operating expenses have to be greater than or equal to rents (DSCR of <=1.0).

Tips:

(1) Speak to your lender and explain your situation

(2) Obtain a broker’s valuation of the building

(3) Keep servicing debt owed

Advice to NYCB Shareholders

Flagstar Bank, or NYCB as I call it, will invite increasing levels of scrutiny as the clock moves closer and closer to loan maturities. 2025 will already put pressure on the lender as maturities increase 120% from 2024 levels. Further, the company will face challenges in its loan portfolio with no apparent solution – absent both a reversal in the 2019 legislation and a reduction in treasury yields.

Though the company tried to diversify away from its rent stabilization business, it has failed to pull the bandaid. The collateral value for half of NYCB’s multifamily loans has been reduced in value by estimates as high as 40-60%, since 2019. That value decline happened suddenly and then gradually increase each year. Many brokers will attest that 5% cap rate sales were successful with 100% rent-stabilized buildings in Q3 & Q4 of 2019. Today that would be impossible – and as a result, the inevitable NYCB loan chargeoff will be far greater than if it had performed it in 2019.

The only idea for raising the value of the loan book's underlying assets would be to work with owners to improve their operational efficiency. But that’s extremely difficult because of the number of borrowers. Short of this, because I don’t see a way to grow the value of NYCB’s RS loan assets, it’s very hard for me to see the company doing well.

Advice for NYCB

The only way my little brain can picture NYCB emerging safely from this quagmire of complex legislation, collapsing collateral values, and high interest rates is for the bank to sell some multifamily loans. Sell them today instead of tomorrow; this week instead of the next, in January instead of February; in 2025 instead of in 2026.

Godspeed and good luck to everyone.

I am bullish on NYC Multifamily. Call me to discuss

Best Regards,

Romain

646 326 2220

Source: SEC Questions for NYCB, NYCB Answers to SEC Questions, NYCB Q3 10-Q

Editor’s Note: I am happy to announce that I have left my post at Greysteel and recently joined the NYC-focused CRE brokerage firm Terra CRG