State responses to insurance costs

Frequency of natural disasters & how states react to the dearth of insurance carriers

The cost to insure property is rising in response to sever weather events in the U.S. In coastal states like Florida, California, Texas, and Louisiana, the insurance problem has come to a head and insurers have taken drastic action. NYC’s record-breaking rainfall on September 29th, thanks to Tropical Storm Ophelia, was a reminder that climate disasters can happen here too. The downpour and flooding happened only two years after Hurricane Ida came to NYC in 2022. The increased frequency of storms in NYC likely means that local insurance carriers will need to contend with the same questions that their peers do in coastal states.

In the face of greater weather damage to housing, insurers are doing what you would expect: hiking premiums, raising deductibles, limiting what policies they will cover, and sometimes exiting markets altogether. With mortgage interest rates close to ~2.5x what they were three years ago and property expenses up in every category, higher insurance costs are a bitter pill to swallow. The situation is so dire that some owners in Florida and Louisiana are electing to sell their properties rather than pay their insurance premiums. Others who have paid off their mortgages are opting to “go bare,” or proceed without any insurance coverage, when faced with +40% increases on their housing costs.

Another contributing issue to rising insurance costs is the elevated litigation risk. According to Bloomberg, “Much of the pressure in New York is coming from multimillion-dollar ‘nuclear verdicts,’ payouts of sometimes more than plaintiffs sought in accidents involving construction work.” The nuclear verdicts in turn are forcing insurers to charge higher premiums because those companies must underwrite greater legal risk in their expense budgets. This is tricky. In 2017, Samari Lakes East, a 635-unit apartment building near Miami, was impacted by Hurricane Irina. The insurer claimed the damage was minor and fell below the annual deductible. Owners of the property sued the insurer and won a $15M payment. While the payment is a win for owners, that insurer will have to raise its premiums considerably the following year to balance out the loss. This creates more distress for property owners.

Florida’s response

Floridian property insurers have been badly hit with natural disaster payouts, but also by mandatory payments to plaintiffs in lawsuits. Only 10% of U.S. home insurance claims are in Florida, yet close to 80% of the homeowner insurance lawsuits happen there. The combination of severe weather patterns and litigation costs have led 7 local insurers to exit the market in the last two years and given Florida the highest insurance premiums in the country. In response, Florida is changing the game in favor of insurers. Property owners can no longer rely on insurance companies to cover their legal expenses for cases they win against them. The change will also force insurers to provide payouts more quickly and promptly and it will also shorten the deadline by when claims need to be filed by property owners. This will make it harder to call out insurance companies acting in bad faith. It will make it tougher for those property owners who struggle to cover attorney fees out of pocket. On the other hand, this legal change should put insurance companies less on edge and blunt the growth of insurance premiums a little bit.

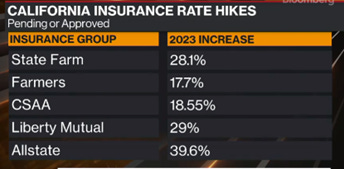

California’s response

In California, seven out of 12 major property insurance companies have retreated from the state (either not underwriting new policies, or greatly reducing what they will cover). Fewer insurance carriers mean that premiums will rise. Further, this leads to gaps in coverage – sometimes in areas that are impacted by wildfires. It’s probably the case that some homeowners are “in the bare.” This is worse than high rates, it’s just 0 coverage. California’s response is to allow the insurers to charge customers more. Previously carriers were only able to price the cost of coverage based on historical data. They will now be allowed to consider forward-looking data as well. In return, insurers must be willing to underwrite ~85% of the areas at risk of wildfires. To offset what is inevitably going to be a higher premium for the homeowner, California lawmakers are in talks to offer discounts to end users if they can implement “risk mitigation factors” to their homes.

What will be New York City’s response?

The rising cost of insurance and the spottier coverage nationally is something that New York will have to contend with as the severe weather patterns and litigation persist. How will the state overhaul its insurance program for owners of multifamily? Homeowners? The same carriers that pay out court ordered fines in California sometimes have presences in NY and those big financial holes need to be plugged by raising premiums – if not here then there. How will NY respond? This is an important challenge that investors buying today should not take too lightly -especially when considering rent regulated properties where revenues are effectively capped.