This Legal Challenge is Different

Narrower scope, and invited by the SCOTUS

Two apartments sit empty at 81 Cabrini Boulevard, a 30-unit prewar building in Hudson Heights. One carries a legal regulated rent of $710 a month. The identical layout one floor below rents for $2,595. The second vacant unit has a legal rent of $860; a comparable apartment one floor up leases for $3,000. The owners, brothers Pashko and Tony Lulgjuraj, estimate that bringing either unit up to code would cost more than $100,000, which is money that would take a very long time for the regulated rent to recoup under current law. So the units sit dark, producing zero income, while a nearly identical unit down the hall throws off well over $30,000 a year. (Institute for Justice complaint, via The Real Deal, Nov. 14, 2025)

That fact pattern is the centerpiece of Small Property Owners of New York, et al. v. City of New York, a federal lawsuit filed in the Southern District of New York in November 2025, and it deserves more of an NYC multifamily investor’s attention than this year’s rent freeze. The freeze, whatever one thinks of it, is an arithmetic event: a known percentage, zero, applied to a known base of roughly one million units, for a known two-year period. While it’s fresh news, well, there were signs of its arrival. As a result, many investors have priced the freeze into their models (at least that’s what we advised them to do). This lawsuit should be thought of differently. It asks a federal court to decide that capping rent increases on vacant, rent-stabilized units amounts to an unconstitutional taking of property (i.e. Fifth Amendment). If it succeeds, the effect on value will not move through the market the way a guideline vote does.

A Brief History

Since the 2019 Housing Stability and Tenant Protection Act, landlord groups have thrown nearly every constitutional theory available at rent stabilization and lost. The template was set well before HSTPA, in Harmon v. Markus, a 2008 case that argued sixty years of renewed “housing emergency” declarations could not sustain rent control indefinitely; the Second Circuit affirmed dismissal in 2011 and the Supreme Court denied certiorari in 2012, reasoning that an owner who buys into a regulated market does so with eyes open. HSTPA then raised the stakes: it eliminated vacancy decontrol (the prior ability to deregulate a unit once its rent crossed a threshold), capped individual apartment improvement (IAI) cost recovery at $30,000 amortized over 15 years instead of a shorter window with no dollar cap, and curtailed major capital improvement (MCI) increases and condo conversions. A wave of takings suits followed, brought by the Rent Stabilization Association and the Community Housing Improvement Program, which merged into the New York Apartment Association (NYAA) in 2023. Each one was dismissed. The Second Circuit affirmed those dismissals in 2024, and the Supreme Court has now declined to hear roughly six separate challenges to New York’s rent law since 2012, most recently 74 Pinehurst LLC v. New York in February 2024, which I covered here and here.

That February 2024 denial carried an unusual footnote. Justice Clarence Thomas, while agreeing not to take up 74 Pinehurst, filed a statement calling the constitutionality of rent regulation “an important and pressing question,”. That’s about as close as the Court gets to inviting petitioners to take a second swing. A close legal read published by Francis Menton in the Manhattan Contrarian in March argues the Small Property Owners of New York (SPONY) case is built to be exactly that vehicle. Every prior case asked a court to unwind the regulatory apparatus for roughly a million occupied units, which put judges in the position of upending frameworks that have been in place for close to three quarters of a century for a population that overwhelmingly (68%) rents. SPONY’s case does not do this. It asks for relief only on units that are already vacant, where there are no tenants to inconvenience or disturb. “We’re not challenging the government’s ability to protect existing tenants,” said Robert Johnson, an attorney with the Institute for Justice, which is representing the plaintiffs pro bono. “When an apartment is vacant, there is no tenant to protect, and it doesn’t help anybody to have these units sit off the market,” according to The Real Deal.

Not everyone buys the distinction in this new case. Ellen Davidson of the Legal Aid Society, which intervened on behalf of tenants in earlier cases and plans to do so again here, dismissed the complaint as “the same thing with new wrapping paper.” She raises a substantive concern: restoring any form of vacancy decontrol, she argues, would recreate the pre-2019 incentive for owners to push out long-term tenants, when “anyone who lived in their apartment for more than 10 years had a target on their back.” City Hall’s position leans on the same fifty-year record of upheld regulation and two Supreme Court denials in the past two years alone.

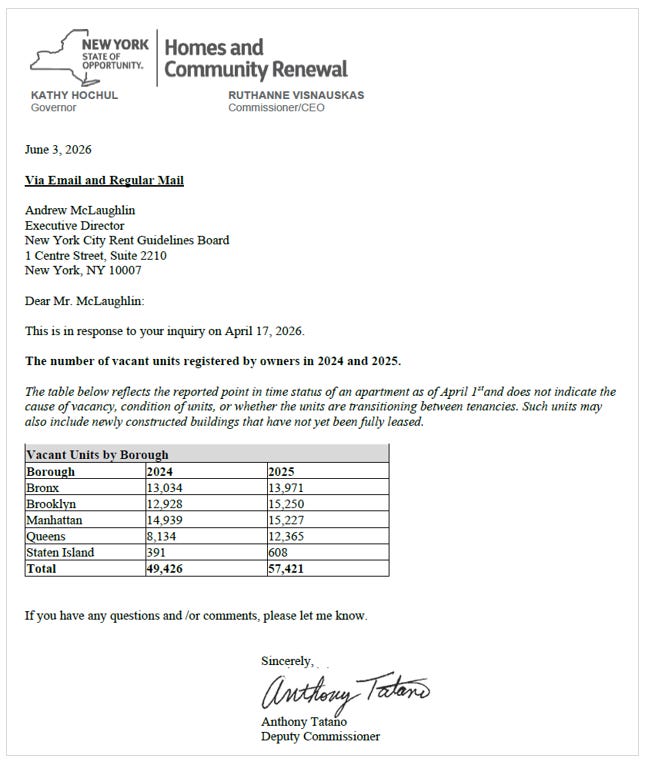

The Cabrini Boulevard units are not outliers. Those watching the sector closely noticed the correspondence between the Rent Guidelines Board (RGB)’s McLaughlin and HCR that highlighted that over 57,000 apartments were registered as vacant rent-stabilized (RS) units last year in 2025. That’s about 5.7% of the RS housing stock, or about 2.5% of all rental housing in NYC (yes, not all these units are unrentable and being intentionally warehoused – so a discount factor must be applied but what a whopping number it is-- approximately equal to 1.5x the housing deliveries in 2025).

SPONY’s complaint adds plaintiffs beyond Cabrini Boulevard, including a six-unit building at 1819 Cornelia Street in Ridgewood and a four-unit building at 135 West 78th Street, each holding units vacant for the same reason. The claims include the Takings and Due Process Clauses of the Fourteenth Amendment, plus Privileges and Immunities and Equal Protection theories, arguing there is no constitutional basis for an identical unit’s legal rent to depend entirely on how recently a city agency reset it.

Option Pricing

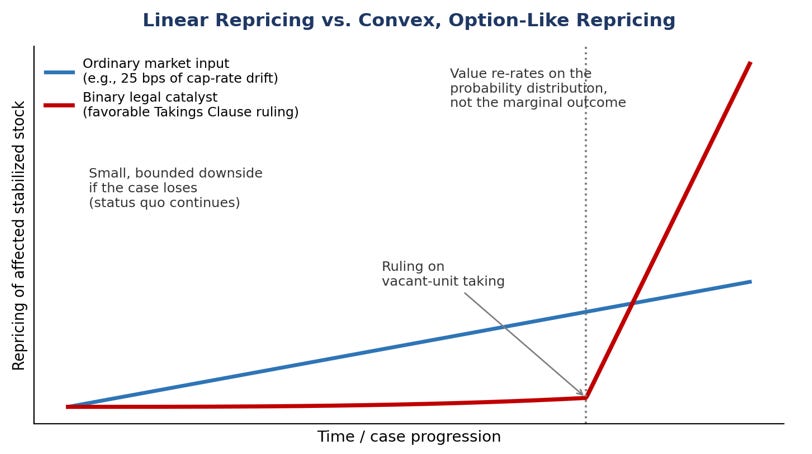

This is where the asymmetric bet framing matters. NYC multifamily investors are pricing risk the way a bond desk prices a small move in the 10-year Treasury: a cap rate assumption shifts 25 basis points, a rent guideline lands at 2% instead of 0%, and value adjusts proportionally, in a line with a modest slope. Litigation like SPONY does not work that way. It behaves like a binary catalyst: it could prompt big change.

Consider how a biotech company is priced ahead of an FDA decision. A clinical-stage drug’s market value is a probability-weighted guess, often assigning single-digit or low double-digit odds to approval. When the FDA clears the drug, especially for a new indication the market had not modeled, the stock does not creep up by the incremental cash flow of that one outcome. It reprices instantly, sometimes doubling in a session (see RETA’s Skyclarys), because the market has to reprice an entire probability distribution at once, not just that drug but every other (pharma) asset in the same class investors now assume is more likely to clear the same bar (for the indication).

Oil exploration runs on the same logic. A wildcat well, or unexplored/untapped oil well, is a complete coin toss: a dry hole is a full write-off of the drilling cost, but a real discovery does not just book that one well’s reserves. It reprices the surrounding acreage, because a single data point changes what the market believes about the entire region/category. ExxonMobil’s 2015 Liza discovery in offshore Guyana turned a country most major oil companies had written off decades earlier into one of the world’s most valuable frontier basins, on the strength of one well.

New technology approvals follow the same shape. A regulator clearing a new technology category, a novel therapy platform, an autonomous vehicle standard, a spectrum allocation, does not just reprice one company’s product. It reprices every asset built on the assumption that the category would eventually be legal to sell.

A favorable ruling in SPONY would not just free two apartments on Cabrini Boulevard. It would establish, as a matter of federal constitutional doctrine, that a below-market legal rent combined with an un-recoupable renovation cost constitutes a taking. It would loosen the caps on cost recovery in place today. And that doctrine would apply immediately to vacant units citywide today, and would extend that same relief, on a rolling basis, to the far larger pipeline of stabilized units that turn over in the future. That is not a linear repricing of net operating income. It is a step-function change in the legal permission set governing a meaningful share of the existing stabilized stock.

To be clear, none of this makes SPONY likely to win. Six prior challenges to New York rent law have failed at the Supreme Court’s door since 2012, and the forces that killed those cases, such as the deference to legislative housing-emergency findings and reluctance to disrupt a fifty-year-old regulatory scheme, remain fully in place. What is different is the fact pattern and the audience. SPONY was deliberately built around the reasoning that ruled out 74 Pinehurst and its predecessors, and it lands in front of a Court whose senior conservative justice has already flagged the underlying question as one worth taking up in the right case.

“…We must consider whether specific New York City regulations prevent petitioners from evicting actual tenants for particular reasons. Similarly, petitioners’ facial challenges require a clear understanding of how New York City regulations coordinate to completely bar landlords from evicting tenants. The pleadings do not facilitate such an understanding. However, in an appropriate future case, we should grant certiorari to address this important question.”

– Justice Clarence Thomas’s statement on 74 Pinehurst LLC et al.

What Investors Should Watch

The motion to dismiss. Case No. 1:25-cv-09425 (S.D.N.Y.) is still at the pleading stage. Watch whether the court lets the narrower “vacant units only” approach survive past the point where standing and ripeness (legal) arguments killed earlier cases.

Any language crediting the as-applied theory. A partial or interim ruling that even implicitly accepts the logic that a below-market legal rent plus an uncapped renovation gap equals a taking matters more than the ultimate remedy, because it reprices the probability of something happening down the road for all buildings, not just the four named plaintiff buildings.

Albany’s legislative response in 2027. The size of any future fix to the individual apartment improvement cap will signal how seriously the state takes its own litigation exposure. A token increase, like the modest bump included in last year’s state budget, suggests Albany is betting SPONY loses; a substantial fix would suggest otherwise.

Pricing of chronically vacant, deeply below-market stabilized units. Watch whether brokers begin marketing this subset of inventory with any premium for optionality ahead of a ruling, the way distressed-debt buyers price litigation reserves into claims trading.

The next cert petition. If SPONY loses at the circuit level, watch for a petition that explicitly invokes Justice Thomas’s 2024 statement. That would be the clearest signal yet that this case, or one shaped like it, is aimed squarely at the Supreme Court.

Final Comments

The outcome of SPONY’s case won’t come down to a coin toss, and underwriting a single building acquisition on the assumption that it wins would be a mistake. But I would not ignore the case the way most of the market currently does, either. It is a long-dated, low-cost option sitting inside the stabilized stock that few are pricing into today’s cap rates. The right way to treat this legal optionality is the way a biotech investor treats a decision date on a drug they do not own much of. Check the docket periodically, understand exactly what a win unlocks, and recognize that if it comes, it will not show up as a 25 basis point cap rate move. It will recast the asset class entirely, and that gap between what the option is worth and what the market is currently paying for it is the actual story here.

For more guidance on how to think about this more clearly, or for updated valuations on existing assets, please reach out to us.

I am bullish on NYC multifamily.

Best Regards,

Romain Sinclair

646 817 4784

Sources

The SPONY Case:

Small Property Owners of New York, Inc. v. City of New York, No. 1:25-cv-09425 (S.D.N.Y. filed Nov. 12, 2025). CourtListener.

Justice Thomas’s Dissent on 74 Pinehurst LLC:

74 Pinehurst LLC v. New York, 601 U.S. (2024) (Thomas, J., statement respecting denial of certiorari).

Real Deal article explaining case:

Brenzel, K. (2025, November 14). Landlords sue New York over rent-stabilization rules for vacant apartments. The Real Deal.