What I Look For In A Rent Roll

There are rent rolls you can defend. And then there are rent rolls that leave you defending yourself. I’ve underwritten enough of these to know that the difference between a long-term winner and a litigation-prone headache usually shows up in the DHCR printout—if you know what to look for. Below, I break down the key signals I watch for in a rent roll and offer three visual case studies to help you spot the good, the bad, and the risky.

1. Defendable Rent Increases: The Blessing & the Curse of Recorded Growth

What makes a rent increase defensible? Timing, recordkeeping, and consistency.

Big jumps in rent aren’t inherently bad—especially if they occurred pre-2019, when the HSTPA rewrote the rules on how and when a unit could exit stabilization. In fact, well-documented bumps in the pre-2019 era can be an investor’s best friend. They suggest improvements were made, that DHCR filings were correctly handled, and that there's a paper trail to fall back on in case of scrutiny.

But post-2019, everything changed. Rent increases are tightly capped, and any large leap will invite regulatory attention. If you see big rent jumps after 2019 without rock-solid records, that’s a red flag.

The best-case hybrid (RS/FM) buildings are the ones where:

Renovations happened before 2019,

Rent increases were recorded with DHCR,

Units transitioned to FM with clear, stepwise logic—not magical leaps from $1,000 to $3,000 in one year.

The irony shouldn’t be lost on investors that ten years ago, these rent bumps were a badge of success. Today, they might be investors’ biggest liability. The very mechanism that made someone rich may keep them stuck in their deal. (Cashed out too much money via refi, and now building worth less than loan balance? Call me – 646 326 2220)

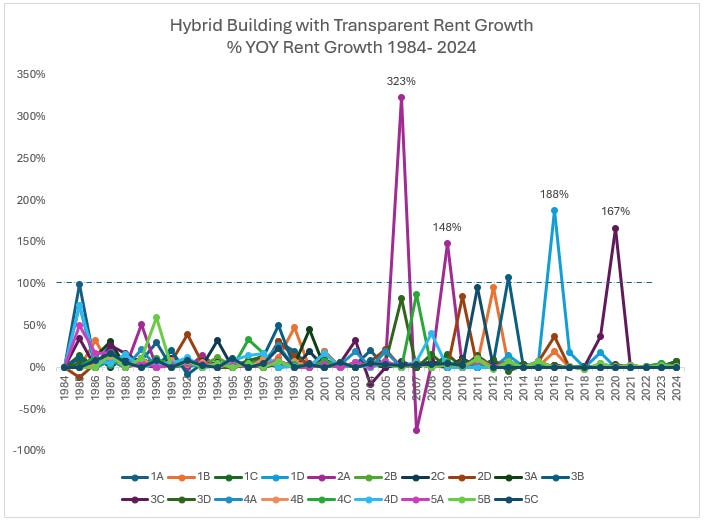

Case Study #1: Hybrid Building with Transparent Rent Growth

Clear rent increases, consistent records, and a defensible path to FM

Takeaways:

Renovations and increases are well-paced and mostly pre-2019.

DHCR filings show documented growth year over year.

Units that transitioned to FM did so from elevated stabilized rents—giving investors a higher fallback if challenged.

High trust in sponsor’s recordkeeping is critical.

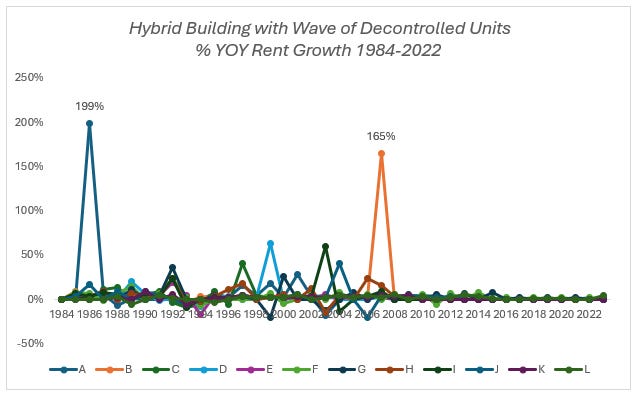

Case #2: Hybrid—But All-at-Once Free Market

Hybrid Building with Big Burden of Proof

This building saw most of its units exit stabilization between 2008–2012. Hard to tell right? Yeah that’s because no intermediary steps were taken to raise rents while still in stabilization. Units were improved and decontrolled in one step. Free market units are always good for investors. But, because the decontrolling of the units happened around the same period, more weight than usual is going to be placed on whether the property has the appropriate records. The burden of proof is high here and will adversely impact value if it’s not all there. Applying common sense helps here.

If I trust the sponsor, I’m good. If not, I walk.

Takeaways:

Risk lives in paperwork. Without IAIs and old leases, you could face a rollback.

The timing of deregulation (2008–2012) is favorable—past the 4-year challenge window.

Safe if records are tight. Dangerous if they’re not.

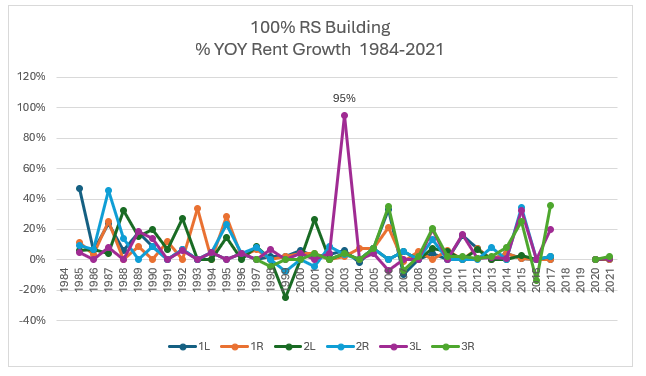

Case #3: Gradual, Rent Stabilized, Slow Burn

Defensible? Absolutely. Profitable? Maybe

This is the gold standard for stability—classic rent-stabilized housing with decades of modest increases. Apartment rents are low. Tenants don’t move. Overcharges are rare. But your NOI will be eaten for lunch if expenses outpace rent growth and if youre tenants skip rent payments—and these tenants can’t absorb much more rent in 2025’s inflationary, tariff-y world.

Takeaways:

Defensibility is top-notch—low risk of overcharge.

But these tenants are vulnerable. Arrears are a real issue.

Watch your OPEX. With 55%+ of income going to operating costs, you’re one bad tax year away from red ink.

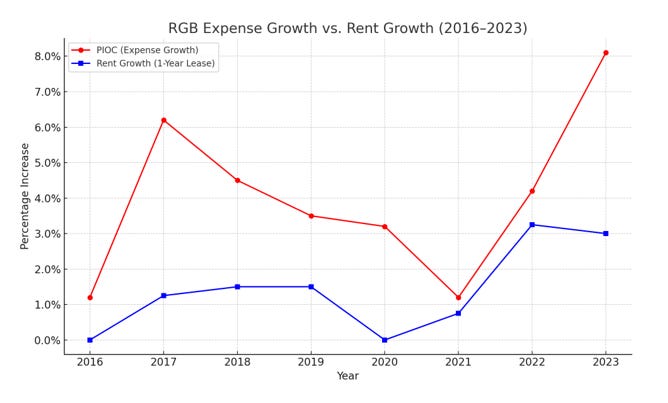

2. Expense Growth vs. Rent Growth

It’s hard to speak about a rent roll without talking about expenses. Because if rents aren’t rising faster than OPEX, NOI is shrinking.

From 2016 to 2023, NYC expenses, especially property taxes and fuel—have grown faster than allowable rent increases in many years. According to the Rent Guidelines Board’s Income & Expense studies:

Expenses grew by 8.1% from April 2022 to March 2023, outpacing rent increases in RS buildings.

Fuel Costs: Rose by 19.9%, the largest increase among all components.

Property Taxes: Increased by 7.7%, primarily due to higher assessments for Class Two properties.

Operating expenses consumed nearly 63% of rental income, leaving a narrower margin for NOI

If your building’s rent roll isn’t outpacing expenses by a wide margin, you’re not buying income—you’re buying liabilities. This is something to be especially weary of because the RGB allowed rent increases in the last 8 years have all been lower than the average increases in operating expense.

3. Rents Below Market in Good Markets

Stabilized units should be deeply below market and ideally be bought in good locations. I like to see blended rents that are 50% or less than what market units in the same zip code command. This acts as the insurance policy. It ensures strong demand and lower turnover. Further, buying below market rents grants investors the optionality for massive upside if the rent laws shift again.

In high-rent zip codes, that means your $1,200 rent-stabilized unit competes with $3,000–$3,500 renovated ones. That’s how you protect yourself against downside—and even find upside.

I walk away from rent rolls that:

Show big rent bumps after 2019 with no documentation

Have free market units created without a trail of stabilized increases

Don’t exceed the buildin’g historical expense growth

Or present rents too close to market in subpar buildings.

The historical rent roll is the most honest story your property will tell. It’s a narrative you can’t rewrite after you buy a rent-stabilized building. So take a close look at it!

Click below to check out an event I am hosting in the coming weeks with great speakers.

I am bullish on NYC Multifamily

Call me at 646 326 2220 to discuss

Best Regards,

Romain Sinclair

Keep reading with a 7-day free trial

Subscribe to Romain Sinclair's NY Multifamily Newsletter to keep reading this post and get 7 days of free access to the full post archives.