Mamdani’s Hold on Real Estate is Overstated

The day after NY Assemblymember Zohran Mamdani won the mayoral primary, share prices of publicly traded real estate companies plummeted. Billions of dollars of equity investments were wiped out. Some capital markets voices have made the case for leaving NYC altogether if Mamdani wins. But how much of this is real versus noise? To figure that out, let’s start with the claim that the markets are already reacting.

The Public Market Response to Mamdani

In my previous piece, I explored some of the consequences that would take hold if Mamdani’s rent freeze plan went into effect. This week, I want to consider whether the office of the mayor grants Mamdani the powers necessary to make his plans come true. Understanding this will be critical for separating real concerns from exaggerated fears.

In this vein, I want to correct some false news that’s been floating around about the public market’s response to Mamdani’s victory. In a Bloomberg article titled “Mamdani’s Shock Win Has Wall Street Fretting Over ‘Hot Commie Summer,’” the author writes:

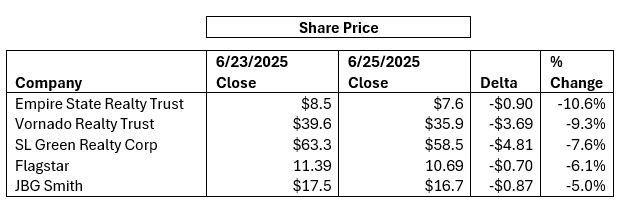

“(…) stocks of companies tied to New York City real estate are getting hit. Flagstar Financial Inc., a lender to apartment buildings, dropped as much as 6.7% on Wednesday before paring its decline to 5%. Corporate landlords Empire State Realty Trust, SL Green Realty and Vornado Realty Trust all fell.”

Share prices in these companies did sharply decline on June 25th, the day after Mamdani asserted victory in the mayoral primary. But what Bloomberg’s account fails to highlight is that the decline took place over several days leading up to, during, and after Federal Reserve Chairman Jerome Powell’s Semi-Annual Monetary Policy Report to Congress. In his address, Powell did not deliver positive news. Though he held the door open for two 25 basis point rate cuts this year, he announced that he was not cutting rates anytime soon as he waited to understand and see the inflationary outcomes of the trade wars and tariffs. That’s bad news for all real estate professionals and arguably worse for NYC real estate professionals than Mamdani becoming mayor.

So, the slump likely had more to do with Powell than Mamdani. But consider the acute decline in JBG Smith’s share price. JBG Smith is a multifamily and office developer that focuses exclusively in the D.C. and Mid-Atlantic market. It has no properties in NYC. That its share price fell as much as that of NYC-focused firms like SL Green tells us something. It’s understandable that investors linked the 6/25 slump in NYC firms to Mamdani. But, it doesn’t make sense to blame Mamdani for a slump that affected real estate firms with no ties to New York.

Still Mamdani’s platform has spooked many in finance, especially those focused on rent regulation. According to PUCK, a “fretful Wall Streeter” wrote:

“If you struggled with what might trigger a fiscal crisis like ’75, struggle no more. Mamdani (with the negligent acquiescence of Albany) will drive the tax base out of NYC by taxing the rich and upper middle class to Florida, and degrading real estate values with more rent control. Deficits will balloon with spending schemes. Ratings agencies will downgrade NYC. Municipal bond markets will rebel. D.C. will punish the city with revenue cuts. Tighten your chinstrap.”

This kind of rhetoric is understandable, but it also deserves a reality check. While the public’s perception may have been exaggerated, the underlying concerns about Mamdani's impact on real estate aren't entirely baseless. The key question isn't whether his policies could affect the market, it's whether the mayor’s office would grant him the power to implement them. To separate signal from noise, it is helpful to understand what the mayor of NYC can actually do.

NYC Mayoral Powers & the City Budget

Mayors in NYC have four explicit powers they can wield to introduce laws and make change happen. Those are:

1- Budget Setting

2- Issuing Executive Orders

3- Veto Power Over Legislation

4- Appointing Power & Rule Enforcement

Out of the four levers of power, the ones that would further Mamdani’s agenda are mostly going to be budget setting and appointing power. The budget-setting power of New York City mayors is a critical tool for advancing mayoral priorities, as mayors propose the city’s annual budget, negotiate with the City Council, and leverage their influence to allocate funds strategically. Ongoing control over capital allocations to city agencies is also important because it keeps agencies beholden to the Mayor’s office and his priorities.

Mayor Adams has been effective in using these tools to tackle the affordable housing issue in NYC and his success shines a light on what can be done from the mayor’s seat. Adams used his budget-setting power to support his “City of Yes for Housing Opportunity” (COYHO) zoning plan, allocating $5 billion in city funds from the NYC budget ($112.4bn in 2025), and securing $1 billion in state support to further the goal of creating 80,000 new homes by 2032. Control over the executive budget allowed Adams to align city finances with his policy goals. Through his control of the executive budget, Adams turned his City of Yes plan from a zoning blueprint into a funded, actionable policy.

If elected, Mamdani would look to the agenda and budget setting powers to pass many of his agenda items. A Mamdani budget means more total spending and increased social welfare allocations. This is where Mamdani would try to earmark funding to support his core thesis of keeping NYC affordable. That means budgeting for his new comprehensive plan for NYC housing, prioritizing funding for early childhood care and education, and making city-owned grocery stores and free bus fares. Separate from the actual budgetary power, the mayor benefits by his or her ability to create narratives around certain projects and frame issues in ways that support their agenda.

When considering budget setting powers alone – real estate owners won’t necessarily suffer if Mamdani ends up setting the executive budget next year. The prospective Mamdani administration wants to create a housing plan, prioritize early childhood education and care and focus on some livability and affordability measures for New Yorkers. That does not mean lower rents or higher expense for owners… does it?

Well, to pay for additional services, additional funding will be needed and that could actually mean higher property taxes. In fiscal year 2025, NYC property owners paid $33.7 billion in property taxes, which made up 30% of the city’s total budget of $112.4 billion. When considering just NYC tax revenues, property taxes made up 44% of the pie. On the other side of that figure are real property owners footing these bills. It’s hard to think of a conversation I’ve had (and I have a lot) where an investor didn’t complain about the surge in their property taxes in the last few years. That’s likely because NYC’s budget has risen nearly every year since 2012 (see below). One of the main problems with a Mamdani mayor is the concern over rising property taxes. Investors already view property taxes as major drain on building operations at 30% of gross rents, and many worry that they will swell even higher.

The silver lining for investors is that it would be very difficult for Mamdani to use the city budget to make changes to rent stabilization law (RSL), good cause eviction (GCE), or property tax abatement policies in ways that hurt property owners, because these are all state-level laws. These are the policies that really matter for investors. Short of using soft power and lobbying legislators, the NYC mayor has no direct tools he can use to affect these policies.

*Cue collective sigh of relief*

Other Mayoral Powers

Mayors can issue binding Executive Orders (EOs) to achieve targeted outcomes such as establish or reorganize city offices and task forces, set administrative procedures for agencies (e.g., climate planning, procurement rules), direct how laws are interpreted or prioritized for enforcement, or declare emergencies or suspensions of certain rules. Mayor Adams used this tool when he issued Executive Order 43 “requiring city agencies to review their city owned and controlled land for potential housing development sites.” This EO is supposed to unlock publicly owned real estate for development. Vacant lots, defunct warehouses, and even parking lots under city control will be inventoried for potential rezoning or RFPs for affordable and mixed-income housing. This should increase transaction flows and eventually spur more construction across all boroughs, addressing the housing shortage and transforming underused land into apartments.

The veto power of New York City mayors allows them to reject legislation passed by the City Council, forcing a two-thirds supermajority (34 of 51 votes) to override. This power is a key tool for shaping policy by blocking or delaying initiatives that conflict with a mayor’s agenda. Mayor Adams used this when he disagreed with the city council over eligibility requirements and how much funding to assign to City FHEPS, the voucher program that places formerly homeless folks into homes. The City Council ultimately overrode Adams on City FHEPS, so using the veto tool has to be done with care. This won’t be a huge part of the next mayor’s toolkit, but it’s something that can be leveraged in very important cases.

Mayoral Appointments & the RGB

Of all the mayoral powers, none matters more to rent-stabilized owners than the power to appoint the Rent Guidelines Board. Mamdani is running on a rent freeze platform, and that poses one of the biggest risks to investors. Elected officials have passed rent freezes before; it is not a novel idea. But what’s different today is that the tools landlords once had to absorb the shocks of rent freezes are gone.

Former mayor De Blasio’s RGB issued rent freeze orders in 2015, 2016, and 2020 in response to COVID-19. The key difference between then and now is that those rent freezes occurred during an era when investors had various methods of raising rents and were not so dependent on the RGB for revenue growth. These methods included performing major capital improvements (MCIs) and individual apartment improvements (IAIs). While De Blasio was mayor, combining apartments meant setting first rents and getting large rent increases, getting empty apartments meant adding vacancy allowances to rents, and if apartment rents exceeded threshold levels, they became free market.

Now that these additional roads to rent growth have been closed off property owners are having a hard time. Since the passing of the Housing Stability and Tenant Protection Act (HSTPA) (2019), incentives for property owners to renovate apartments and raise rents have evaporated. And that policy shift is only half the picture. The financial backdrop makes a freeze even more dangerous.

Six years later, the landscape of apartment investments in NYC has changed. Buildings have higher expenses-to-rent ratios and loan payments have ballooned thanks to higher interest rates. Deferred maintenance has piled onto these properties and some properties are in distress. Investors are holding their breath for either a change in rent laws or an interest rate cut. That’s the backdrop against which Mamdani’s rent freeze proposal lands. And for owners who’ve been barely covering their debt service, or who have maturities coming due in 18-24 months, a rent freeze is just bad timing. The problem isn’t just the rent freeze, it’s a rent freeze at this vulnerable time for property owners.

But does Mamdani really control the Rent Guidelines Board?

The NYC mayor appoints all nine RGB members, with specific roles for tenant, owner, and public representatives, and holds significant influence, particularly over the chairperson, who serves at the mayor’s pleasure. While the RGB is legally independent and mandated to base decisions on data and public input, the mayor’s appointment power means members may reflect the mayor’s housing priorities, raising questions about true independence. Some believe this will lead to a board that favors rent freezes under Mamdani – and I agree.

By the time the next mayor is inaugurated, eight out of nine (8/9) RGB members will have seen their terms expire, which gives the incoming mayor broad latitude over who to select to carry out his agenda. Does a Mamdani mayoral victory guarantee a rent freeze on rent stabilized apartments? No, it doesn’t. But it makes that prospect highly likely. The mayor has the tools and influence to get a rent freeze done. Though there is a growing body of data about the negative profitability of property owners, the RGB members may just as easily unearth data that talks about what inflation has done to the price of eggs in the last six months. If Mamdani wins, the RGB increase will very likely be lower on average from this year’s 3.0%.

So, How Bad Would a Mamdani Mayorship Be?

Let’s take a step back. Concerns over Mamdani’s potential election to NYC Mayor have in some cases reached doomsday level worries. I have heard firsthand from investors expressing their concerns, and many of their fears are valid. Rent freezes on the one million rent stabilized properties could happen and Mamdani appears to have the conviction and the support from allies to move forward with it. On the other hand, changing the new construction tax abatement code to make all newly built apartments with tax abatements subject to rent stabilization is not something Mamdani can do. This is not something under the city’s jurisdiction, and it is not something the mayor has direct control over. Ultimately, some fears are valid, others overstated. If elected, Mamdani will have a limited number of tools to create change–not a magic wand to rewrite state law or override economic reality.

I am bullish on NYC Multifamily.

Best Regards,

Romain Sinclair

646 326 2220

Sources

1. Goldstein, M. (2025, June 25). Wall Street decries ‘Hot Commie Summer’ after Mamdani surprise. Bloomberg News.

2. PUCK. (2025, June). Political memo excerpt referencing fiscal crisis fears post-Mamdani win. PUCK News (Archived).

3. Citizens Budget Commission. (2024, January 16). New York City’s already high spending keeps climbing. Citizens Budget Commission.

4. De Avila, J. (2025, June 25). Zohran Mamdani’s rent control platform jolts NYC landlords. The Wall Street Journal (Archived).

5. Mamdani, Z. (n.d.). Zohran for NYC: Official campaign platform. Zohran for NYC.